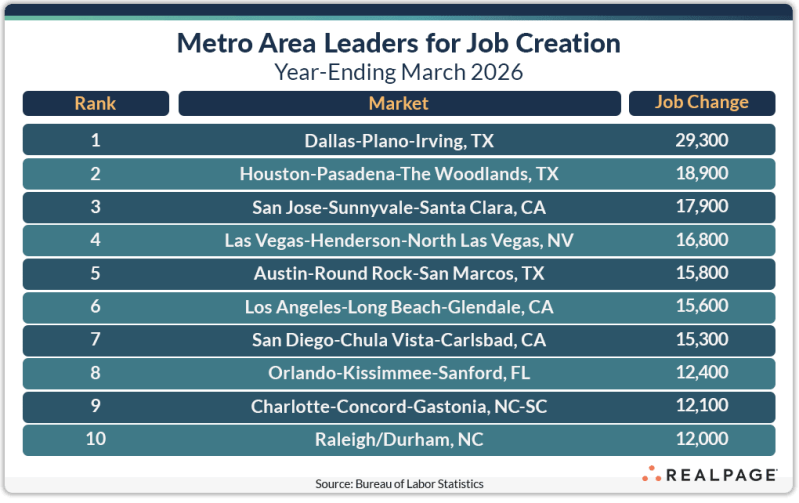

The combined total of new jobs among these top 10 markets (166,000 jobs) was almost 50% greater than their combined annual gains in February and 13.3% greater than one year ago:

On the downside, the Northeast region is facing steep job cuts with 107,900 fewer jobs for the year in Washington, DC, and significant declines in New York, Boston, Baltimore and Philadelphia. The Midwest region was not spared from declining employment levels as Detroit, St. Louis, Milwaukee, Toledo and Pittsburgh also reported job cuts for the year-ending March.

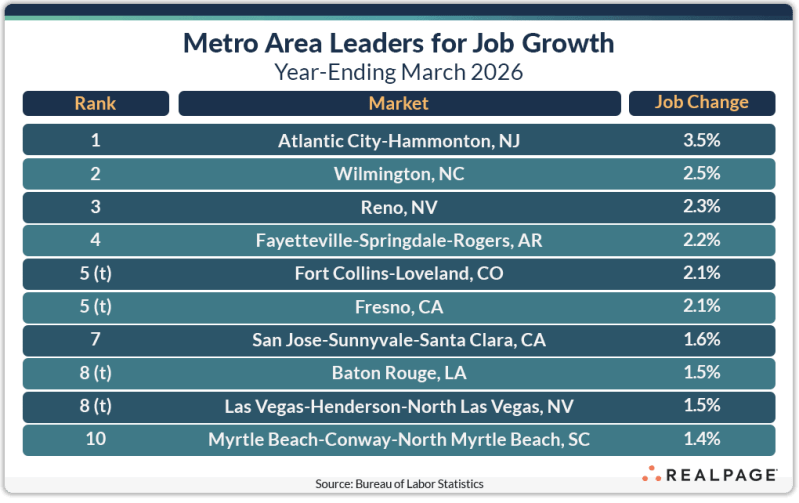

Unlike the top job gain markets, which tend to be large in population and employment, smaller markets usually dominate the top markets for annual percentage change in employment.

Other top 20 large markets in the 1% to 1.1% growth range included San Diego, Dallas, Raleigh/Durham and Austin.

Source: RealPage