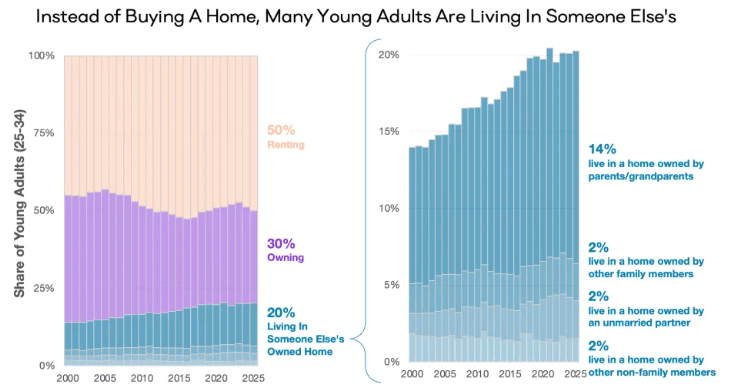

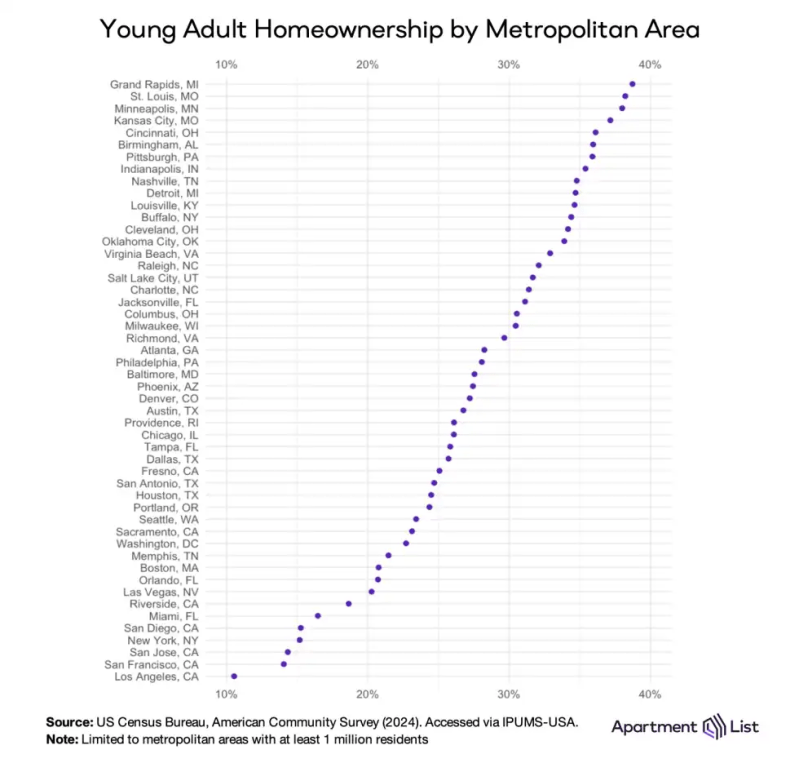

Source: ApartmentList

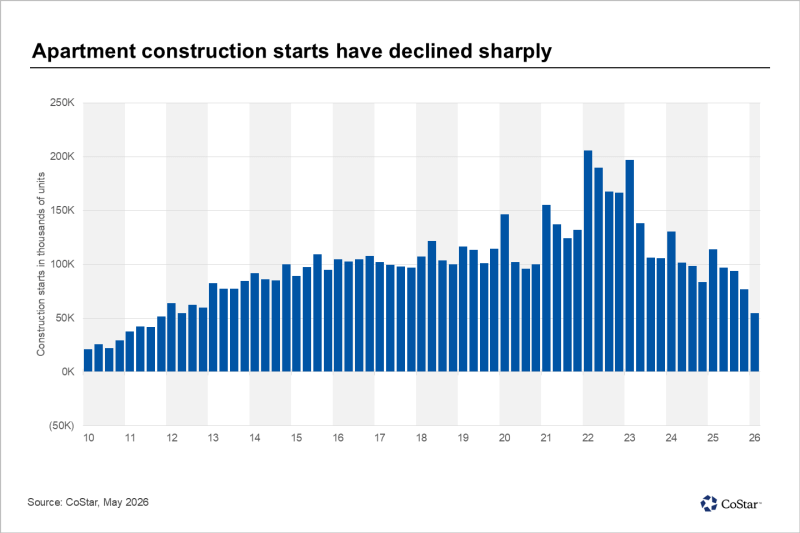

U.S. apartment construction starts declined to approximately 55,000 units nationwide in the first quarter of 2026, a 73% decrease from the peak reached in early 2022 and the lowest quarterly level since 2011.

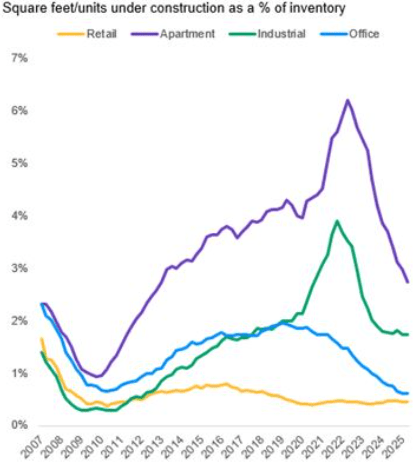

The number of units under construction nationwide declined to roughly 579,000 in the first quarter of 2026, down more than 50% from its peak in early 2023 and broadly in line with mid-2010 levels.

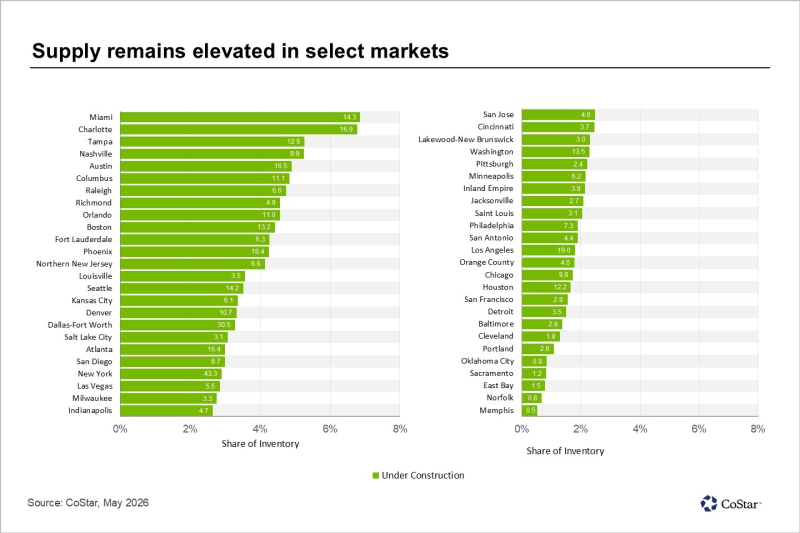

Source: CoStar

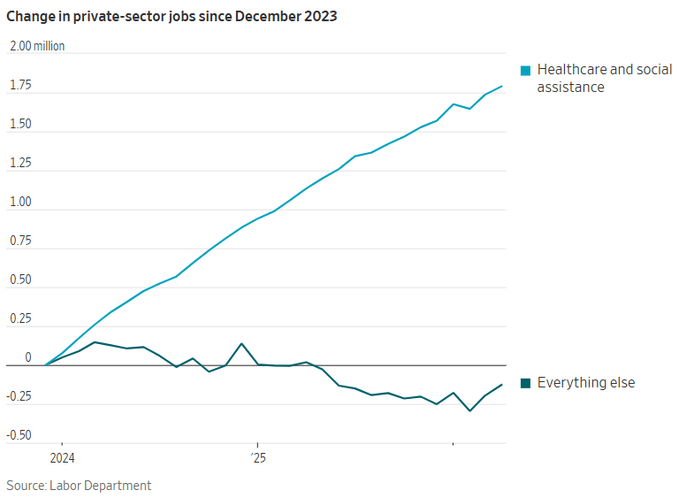

Healthcare and Social Assistance have added nearly 1.8 million private-sector jobs in the US since the end of 2023 while all of other industries combined have lost 127,800 jobs:

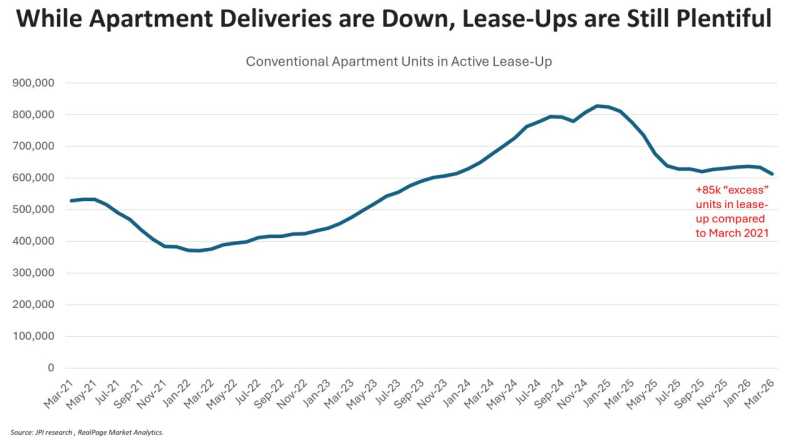

New units that still need to lease-up total 612,000 units nationally. That’s down from the peak of 827,000 units in December 2024, but it’s still about 85,000 units above the baseline from five years ago.

New completions in 2026 are estimated to total about 300,000 units. That’s manageable compared to the 10-year average annual absorption of 350,000 units, but if you add the “excess lease-up” units still to work through, that takes us into 2027 before we catch up … and that’s assuming a normalized absorption rate, which isn’t a given.

Source: Jay Parsons

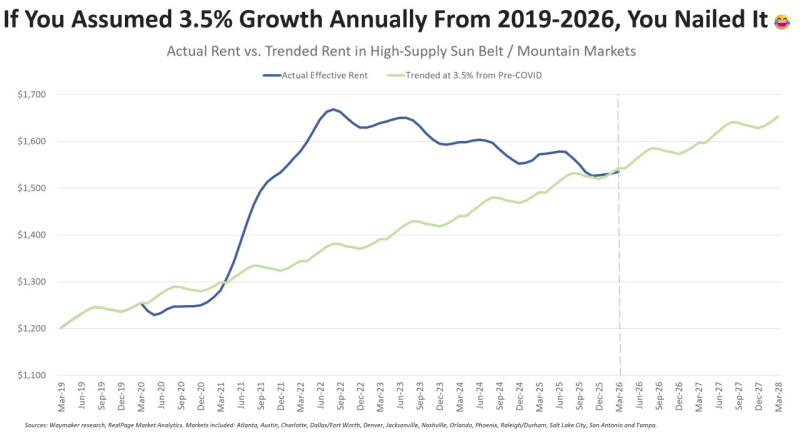

The chart below is a weighted average of the 14 highest-supplied MSAs in the Sun Belt and Mountain markets: Austin, Atlanta, Denver, Phoenix, Raleigh/Durham, Charlotte, Nashville, San Antonio, Dallas, Fort Worth, Tampa, Orlando, Jacksonville, Salt Lake City.

If you bought in a high supply Sun Belt market in 2019 and assumed 3.5% rent growth annually for seven years (light blue line below), you would have been exactly right. That proforma estimate converged with the actual actual path rents took (dark blue line below) this spring.

Source: Jay Parsons

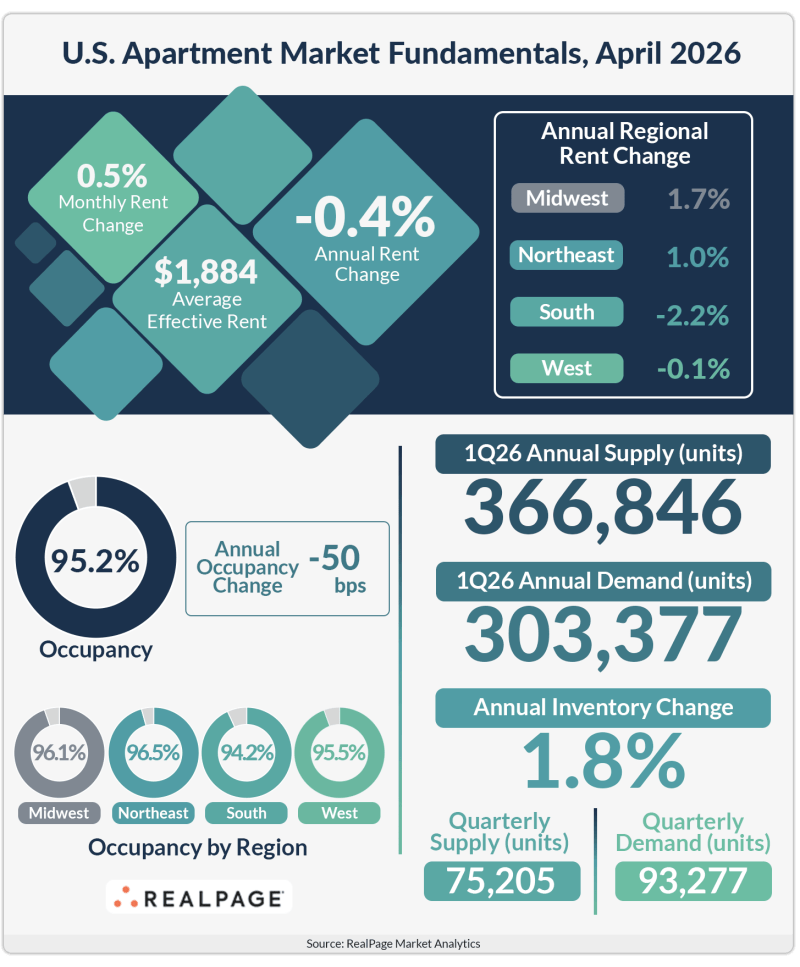

For the first time in seven months, U.S. apartment occupancy rose back above the essentially full mark of 95%.

After steadily declining throughout the back half of 2025, apartment occupancy increased in each of the first four months of 2026. U.S. occupancy hit 95.2% in April, after rising 20 basis points (bps) since March and a total of 60 bps since bottoming out at the end of 2025.

U.S. prices were up 0.5% in April, marking four consecutive monthly increases between 0.2% and 0.5%. That four months of growth, however, couldn’t wipe out previous declines, leaving April rents 0.4% below year-earlier prices.

Source: RealPage

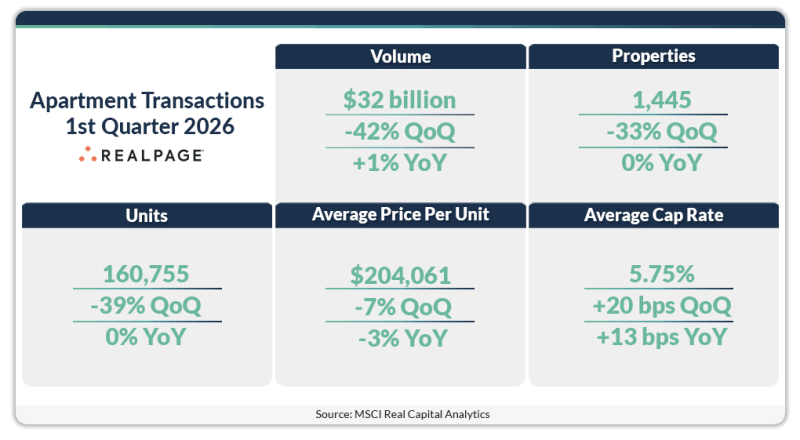

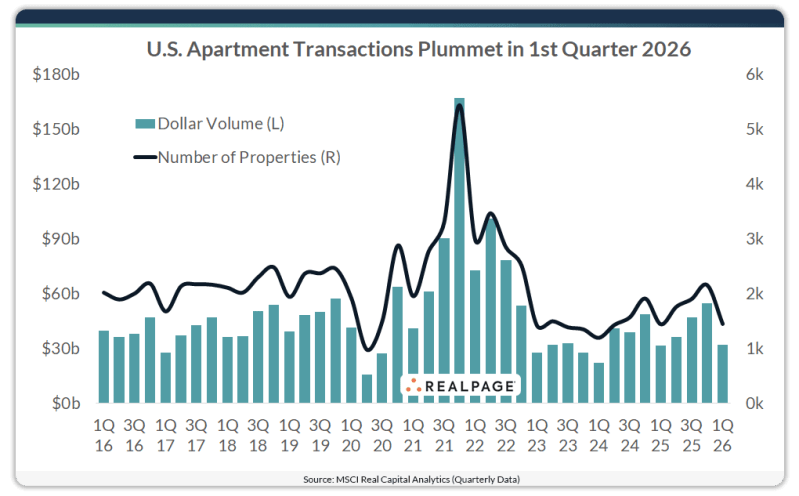

U.S. apartment transactions plummeted during the first quarter 2026, following three consecutive quarters of gains. Both the number of properties traded, and the dollar volume of transactions fell substantially during the quarter.

Overall sales volumes were 42% below the fourth quarter 2025 level, while the number of properties traded dropped 33% during the first quarter. In addition, recent activity was well below the $55 billion quarterly average over the past five years.

Cap rates for apartment transactions occurring in first quarter 2026 averaged 5.75%, well above the pandemic-era low of 4.64% from second quarter 2022.

Source: RealPage

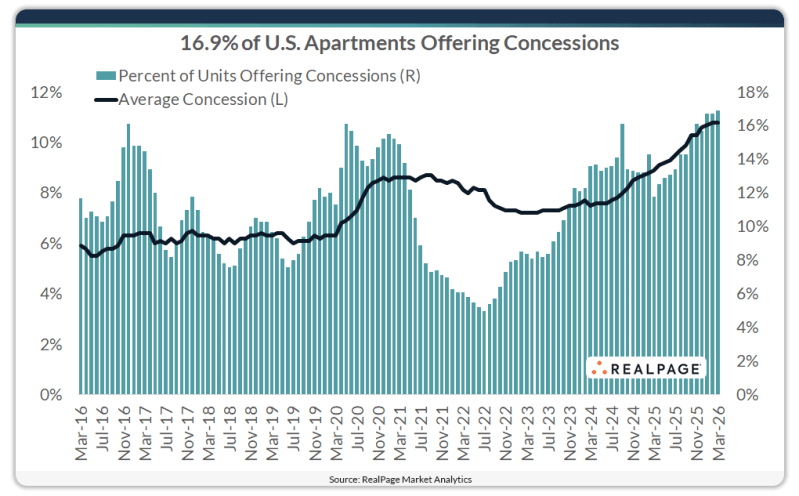

The average discount was 10.8% in March, which equates to six weeks free on a 12-month lease. The number of units offering a concession rose to 16.9%.

Percentage utilizing concessions:

Average discount:

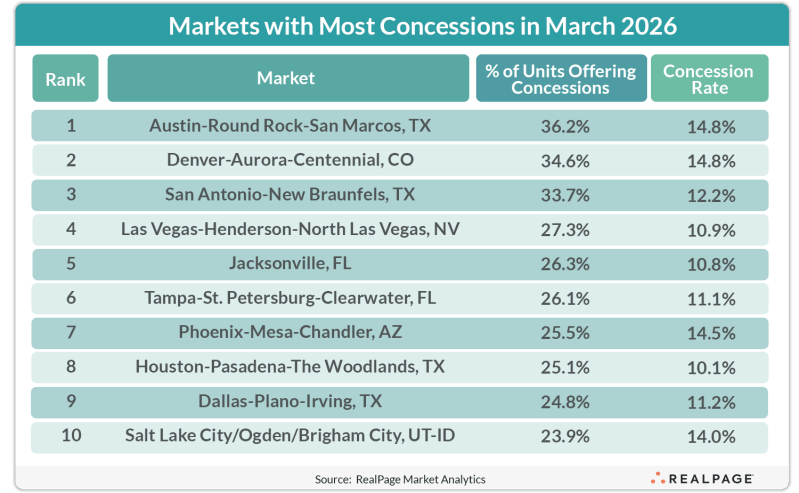

Geographic concession usage:

Source: RealPage

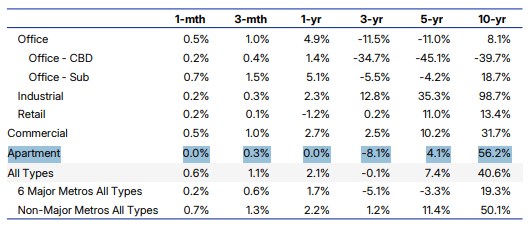

U.S. commercial property prices posted their strongest annual gain since late 2022, with the RCA CPPI US National All Property Index rising 2.1%.

On a quarter-over-quarter basis, the index rose 1.1%, suggesting a faster annualized pace of growth of 4.7%.

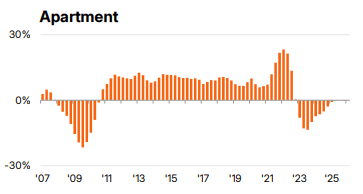

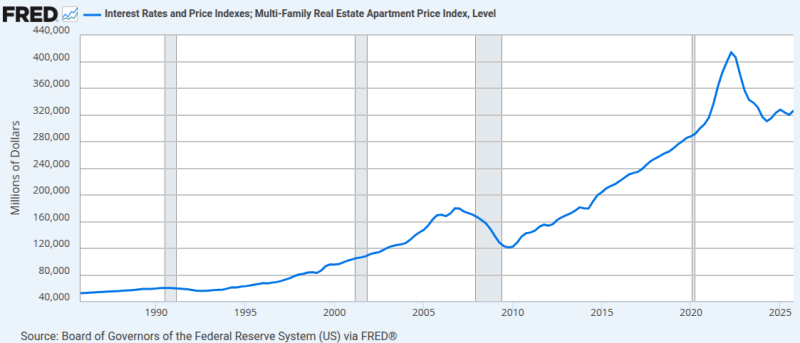

Apartment prices were flat from a year earlier in the first quarter, ending a stretch of annual declines that lasted more than three years. Apartment prices rose 0.3% from the fourth quarter of 2025, suggesting an annualized rate of growth of 1.4%.

The Federal Reserve’s data shows a similar path for multifamily prices:

Source: MSCI