Source: Rentometer

Source: Rentometer

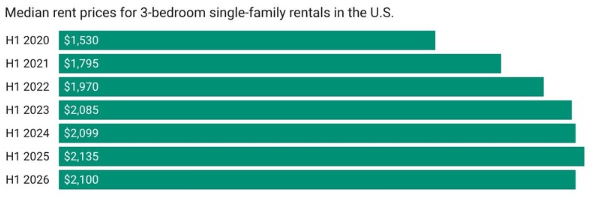

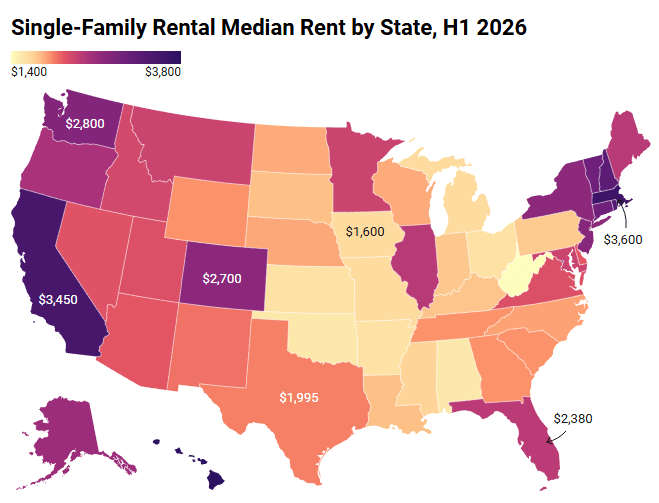

The U.S. single-family rental market continued to cool during the first half of 2026, with the national median rent reaching $2,100, down 1.6% year-over-year.

Rents increased by approximately 1.7% during the first half of 2025 but began declining during the second half of the year, effectively erasing those gains by year-end. That softer pricing environment has carried into 2026.

Another notable feature of the first half of the year was the absence of the typical seasonal lift. The national median rent remained unchanged at $2,100 in both the first and second quarters, even as the market moved through its traditional peak leasing season.

Historically, rents tend to increase during the spring and early summer months as demand picks up. The lack of any seasonal increase suggests pricing momentum remained weak even during some of the year’s busiest leasing months.

Source: Rentometer

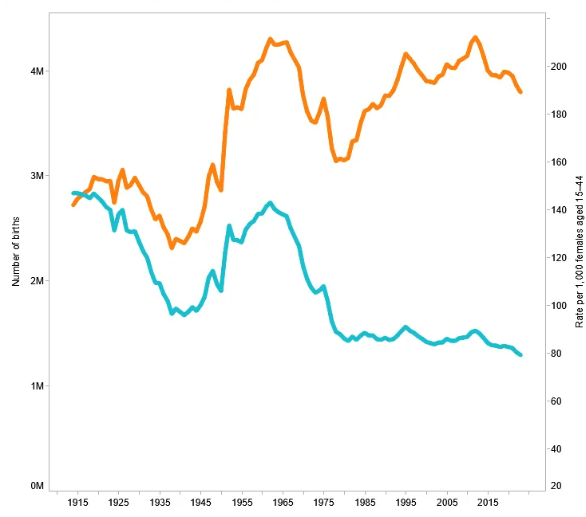

We hit a low point of 2.3 million births in 1933 (following the Great Depression). The babies born during that year are turning 93 this year. The numbers gradually increased after that reaching almost 2.6 million in 1940 and just above or below 2.9 million during the years between 1942 and 1945, babies who are 81 to 84 today.

Then things took off with the number of babies reaching 3.4 million in 1946, the onset of the baby boom, over 4 million by 1954 and a peak of 4.3 million in 1957. They stayed above the 4 million mark through 1964, the last year of the baby boom.

The chart below shows the annual number of births each year in orange (and the birth rate in blue).

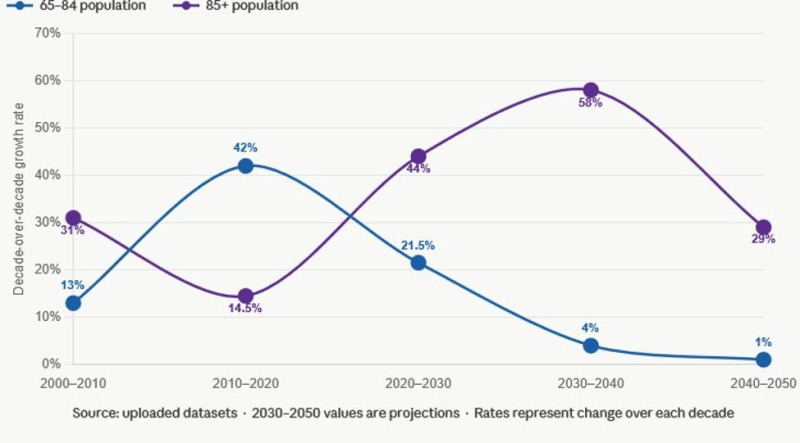

The 85+ group will grow by 44% this decade and will skyrocket by 58% during the 2030’s, before slowing to a more moderate 29% growth rate in the 2040’s.

The number of Americans aged 65 to 84 is only projected to grow 21.5% this decade and then essentially stop growing after 2030.

Source: Harry Margolis

From the Wall Street Journal:

Living at home as a 20-something was once viewed as a failure to launch and even a source of embarrassment in a culture that places a premium on independence. That is no longer the case. Living at home is now often viewed as a sign of financial prudence, and for some, a long-term prospect.

Chronically high living costs are helping reshape the milestones of early adulthood in America. The national median home price hovers above $400,000. Rents are at record highs in cities across the U.S., and many recent college graduates are saddled with tens of thousands of dollars in student debt.

Last year, 49% of adults under age 30 said they lived with a parent, up 12 percentage points from 2019. Nearly a third of those adults were 25 or older.

About 55% of young adults who moved back home said it was out of financial necessity. Far from hiding it, some now broadcast their lives as “stay-at-home daughters” or “stay-at-home sons” on social media.

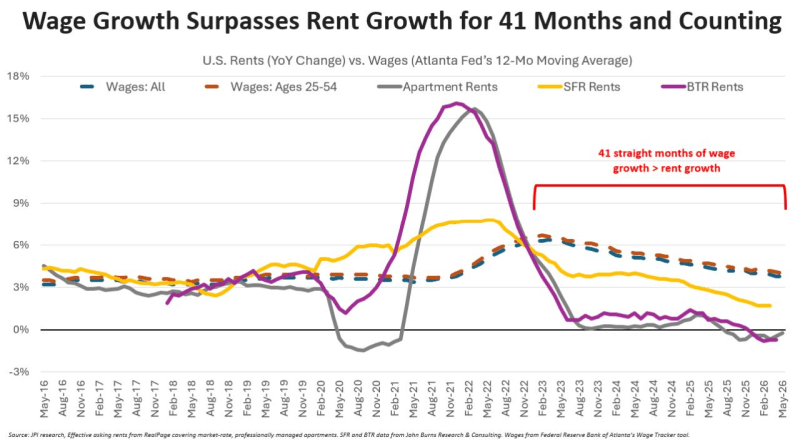

With wage growth outpacing rent growth for 41 consecutive months, rent-to-income ratios are back to pre-pandemic norms around 22%. That’s for renter households signing a new lease in a market-rate apartment.

Source: Jay Parsons

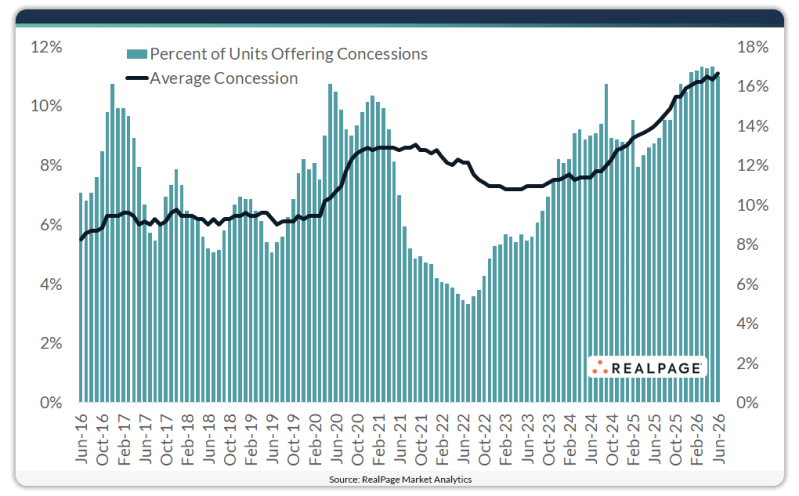

In June, 16.5% of all stabilized units offered concessions, up 3.4 points year-over-year.

The average U.S. concession discount increased 0.2 percentage points month-over-month to 11.1%, marking the deepest discount in more than 25 years. The average discount was also 1.8 points higher than one year ago and translates to nearly six weeks free on a 12-month lease.

Average concession discount by class:

Source: RealPage

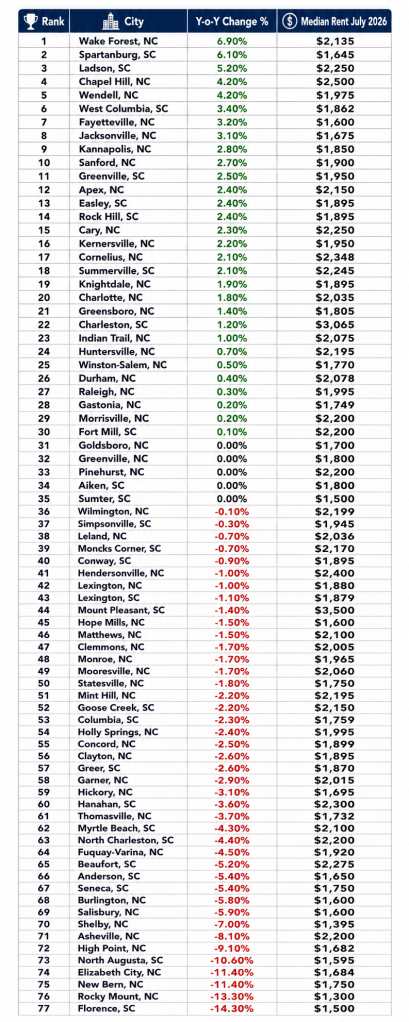

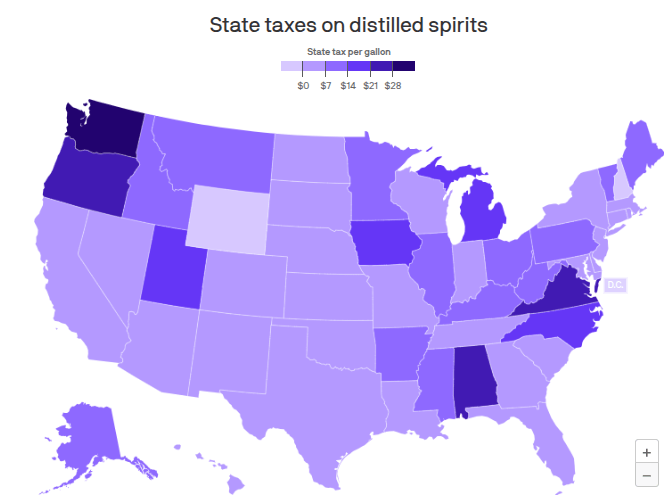

Pretty amazing difference on the NC/SC border:

Source: Axios

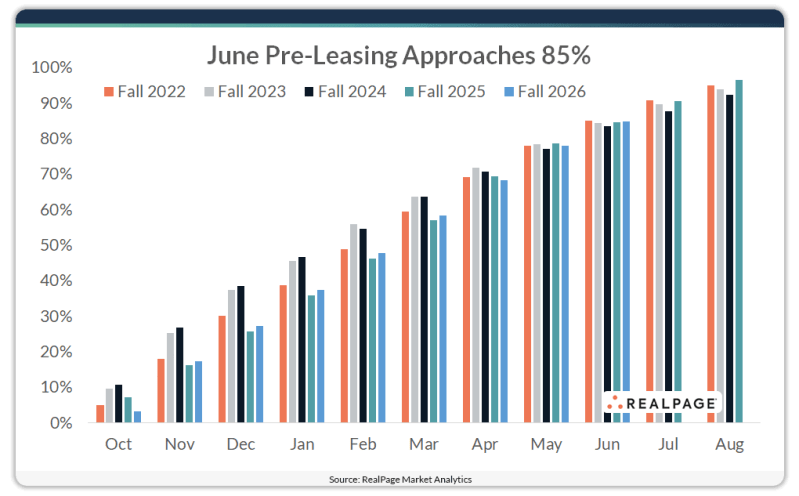

U.S. student housing pre-leasing continued its upward climb in June, with occupancy reaching 84.7% for the Fall 2026 season.

That rate was 340 basis points ahead of the market’s 10-year average June pre-lease level of roughly 81.3% and matched the June 2025 performance.

Source: RealPage

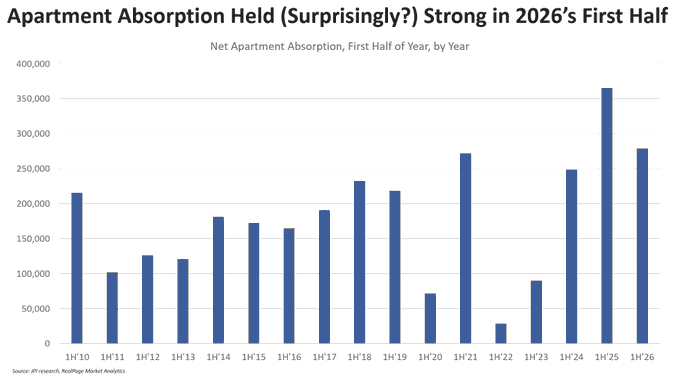

Apartment demand topped expectations in the first half of 2026, with net apartment household formation topping 250,000 units, according to CoStar and Real Page. That’s among the highest absorption starts in history, and it’s better than any year before 2020.

With supply dropping off concurrently, absorption topped supply by about 100,000 units so far this year, reversing a long trend of ultra-high supply topping strong demand. That triggered occupancy growth of 20 basis points in the first quarter of 2026, which was the best for any quarter since 2021.

The absorption trends so far this year are a possible sign that at least one segment of consumers is faring better than generally perceived, especially when these new renters are spending only 21-22% of income toward rent.

Source: Jay Parsons

Apartment vacancies have declined in four straight months, according to Apartment List. That’s the first time that’s happened since 2021. CoStar also reported the Q2 2026 vacancy decline was the largest since 2021.

Source: Jay Parsons