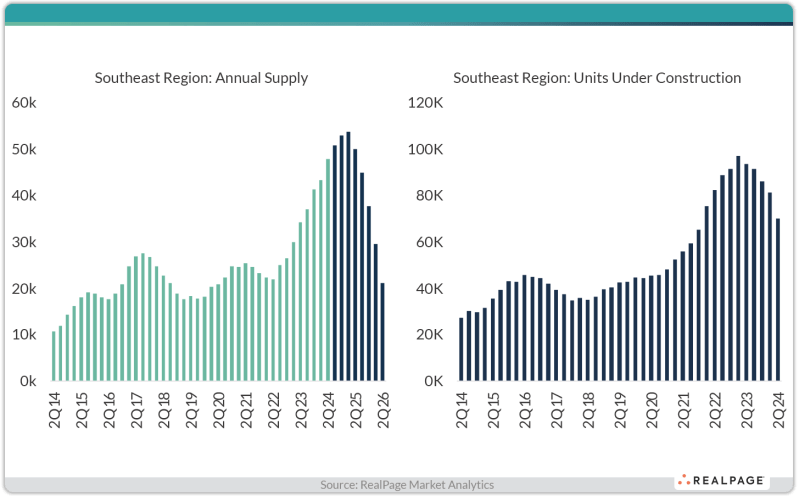

From RealPage: Another 50,000 or so units are scheduled to deliver in the Southeast over the next 12 months, but roughly 10% of that will likely experience a delay, as suggested by historical delivery patterns. With interest rates still elevated, fewer projects have been breaking ground. As a result, new construction activity has been declining for the past few quarters and is set to continue its downward trend in the near term.

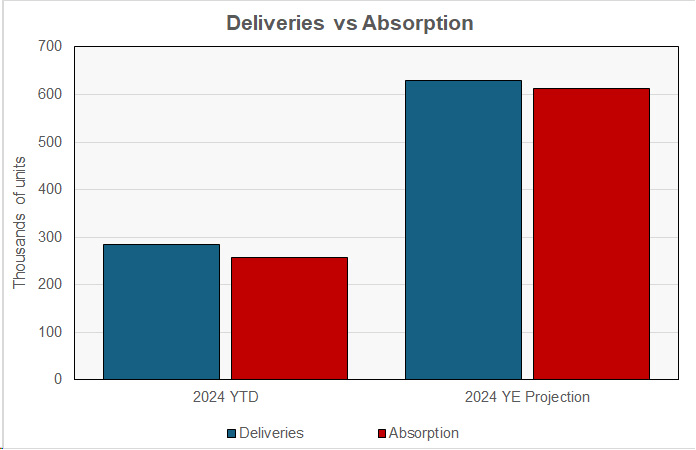

Berkadia anticipates that 2024 will have the highest number of deliveries in this cycle with 283,653 units already delivered in the first half of the year. By year-end, 629,153 new units are expected to hit the market. Berkadia expects net absorption of 612,115 units by year-end, equivalent to 97.3 percent of the new supply. This will result in the current occupancy rate of 94.2 percent rising slightly by the end of the year.

Lease renewals performed better with average rent growth of 4.1 percent in Q2, with 54.3 percent of renters choosing to renew their leases. This renewal rate is up from the pre-pandemic average of 51.7 percent.

The following table gives the mid-year sales statistics for the last 3 years as reported by Berkadia.

Where are Class C rents growing most? In markets with little new supply. Class C rent growth topped 4% in 22 of the nation’s 150 largest metro areas, and nearly all of them have limited new apartment supply.

Most new construction tends to be Class A “luxury” because that’s what pencils out due to the high cost of everything from land to labor to materials to impact fees to insurance to taxes, etc., but when you build “luxury” apartments at scale, you will put downward pressure on rents at all price points.

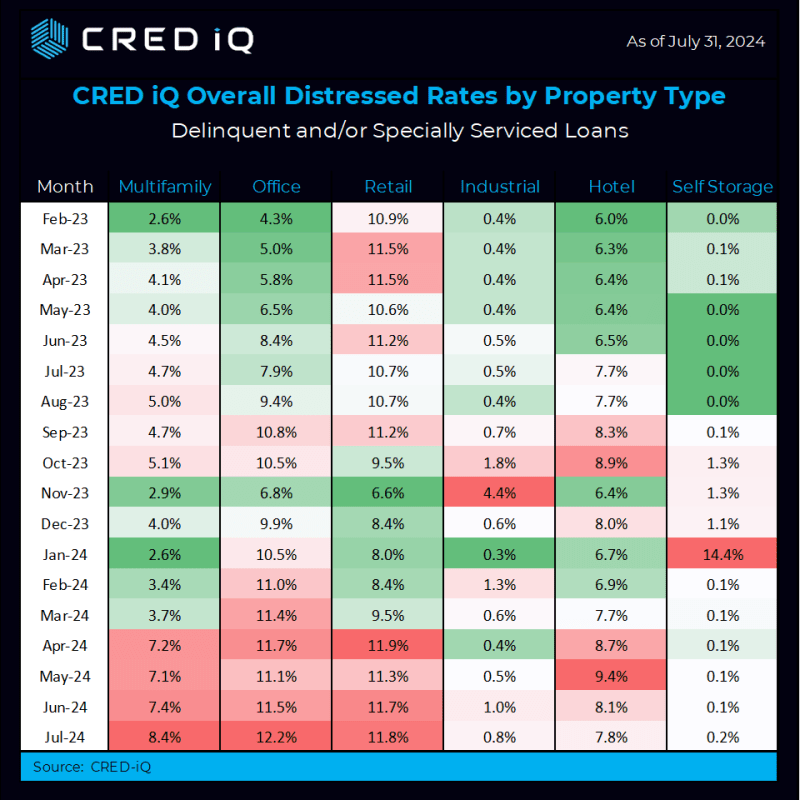

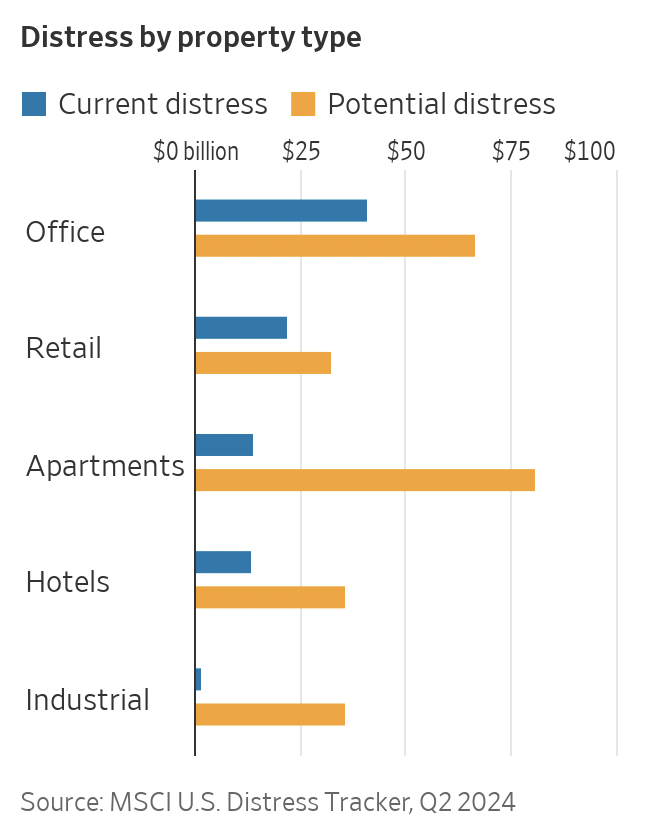

CMBS loans make up a small percentage of the total multifamily debt, but the number of loans distressed within that sector has grown dramatically over the last 7 months.

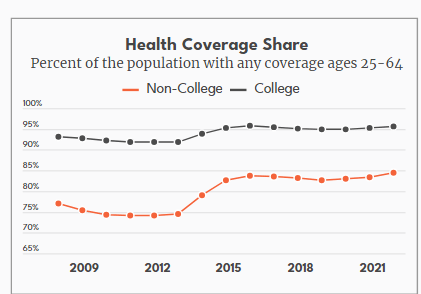

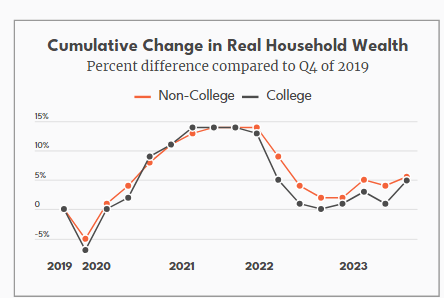

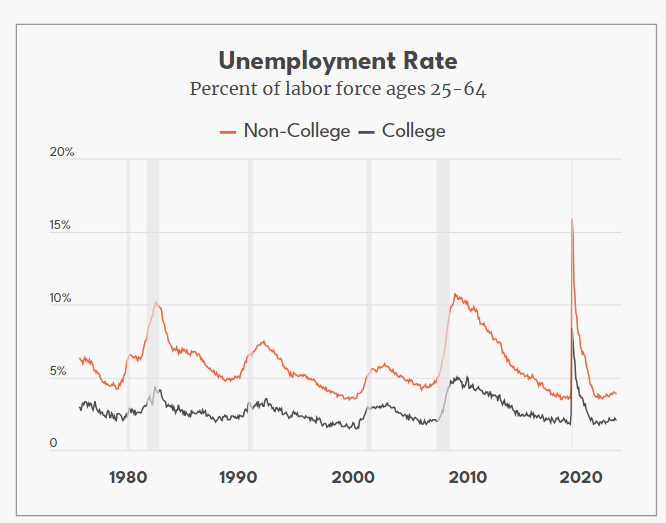

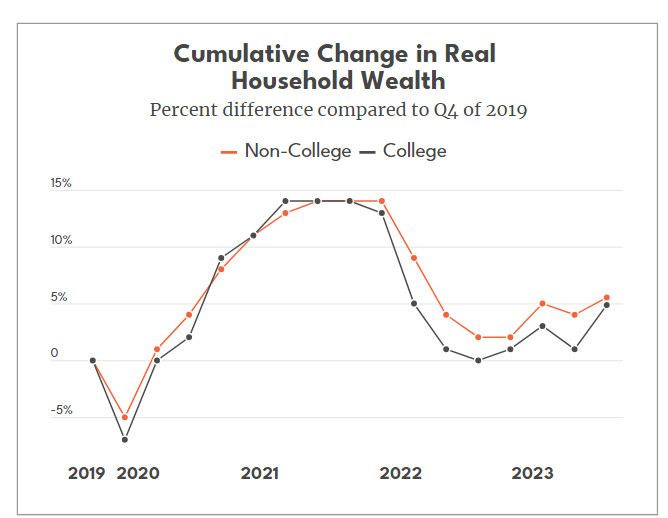

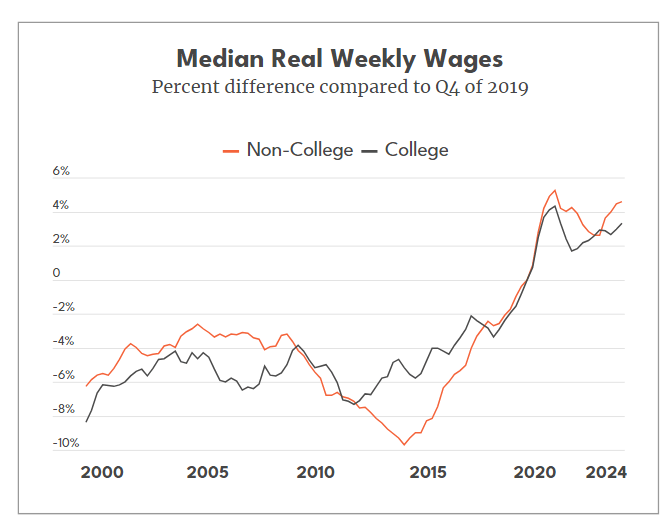

The pandemic recession was an unusual business cycle for Americans without a college degree in many positive respects. Non-college Americans are better off than in 2019 and, in some cases, better off than the hot economy of the late-1990s/early-2000s across a wide array of measures. Many of these Americans start out as renters, which demonstrates why multifamily rents were able to rise so significantly in 2020 – 2022 and have stayed high in most markets.

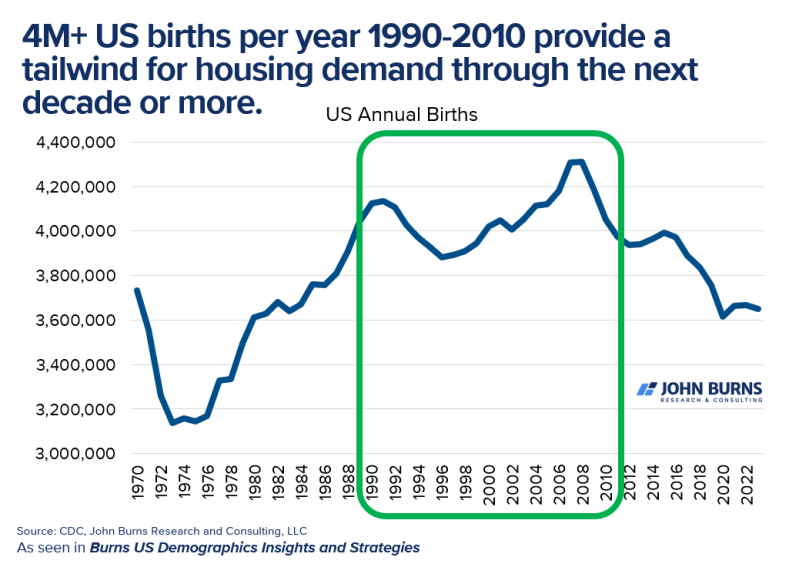

The most common age in the United States is people who are 31 and 32. Births spiked in the 1990s and first decade of this century, peaking around 2007/2008:

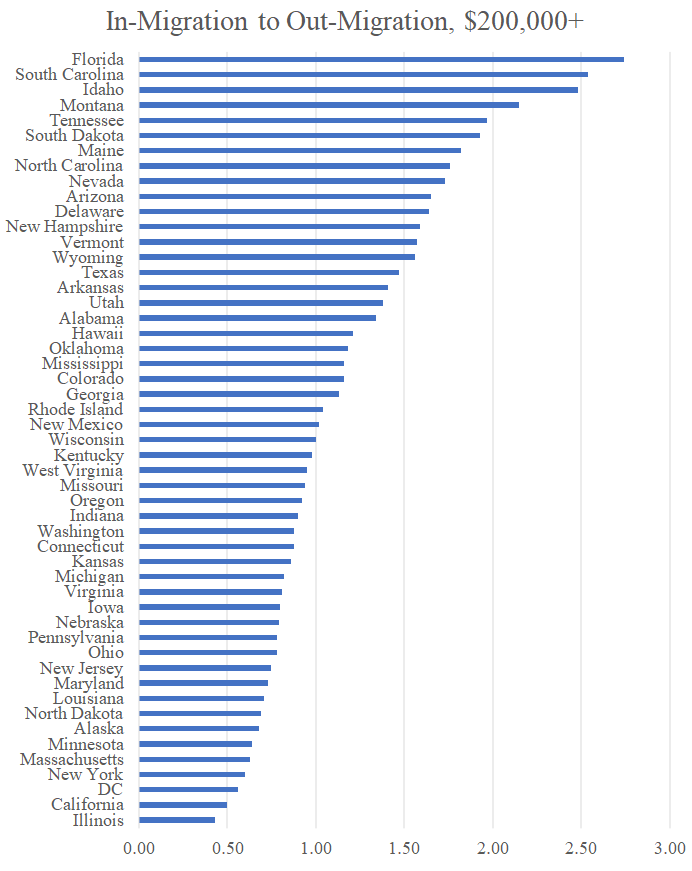

While most of the people in this income bracket will become single-family homeowners, many of them rent for at least a year when they move to a new state.

1.0 is the break-even point (less than that number means you have a larger number of move-outs vs. move-ins).