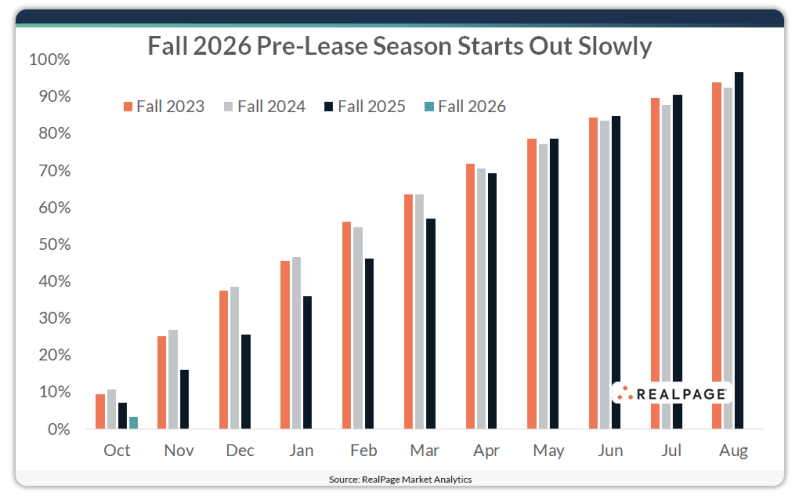

The fall 2026 U.S. student housing pre-lease season started with the slowest October in over a decade with only 3.3% of privately owned student housing beds leased. In the previous three pre-lease seasons, the lowest reading for October was 7.2%.

National apartment rent growth is now projected to decline by 0.1% in the fourth quarter of 2025, a downward revision of 160 basis points from the previous forecast.

Vacancy will stay at 8.2% through year-end, easing only slightly to 7.9% by the end of 2026.

Demand is losing steam. A weaker labor market, slower household formation, and reduced immigration will likely delay absorption in many oversupplied metros.

Lower immigration will continue to weigh on employment growth through 2030, putting long-term pressure on rental demand.

Rents are likely to grow just 1.5% annually over the next five years—below the historical average.

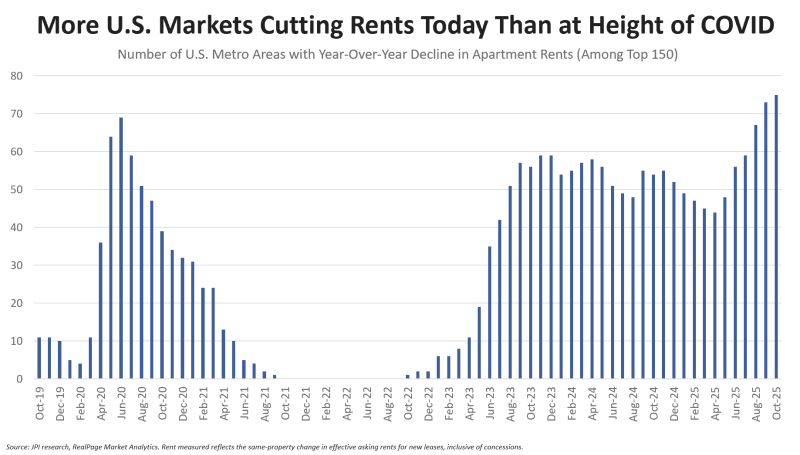

Half of the nation’s 150 largest metro areas cut rents year-over-year through October. Apartment rents are falling in more U.S. markets today than at the height of COVID lockdowns in 2020.

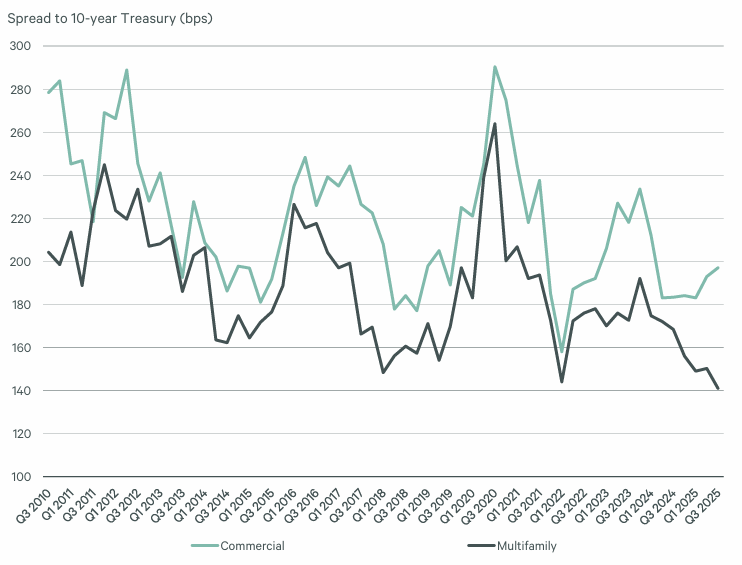

The lending environment for multifamily properties showed meaningful improvement during Q3. Multifamily loan spreads tightened by 27 basis points year-over-year to 141 basis points, driven primarily by lower agency loan spreads.

Government-sponsored enterprise (GSE) lending increased dramatically in Q3. Agency origination volume jumped 53 percent quarter-over-quarter and 57 percent year-over-year to $44.3 billion. The average GSE fixed mortgage rate for closed permanent loans with seven-to-ten-year terms fell 13 basis points during the quarter and 27 basis points year-over-year to 5.6 percent.

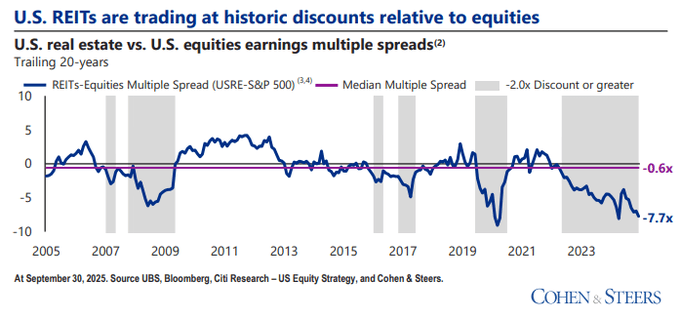

Multifamily loans spreads have diverged from the rest of commercial property loans:

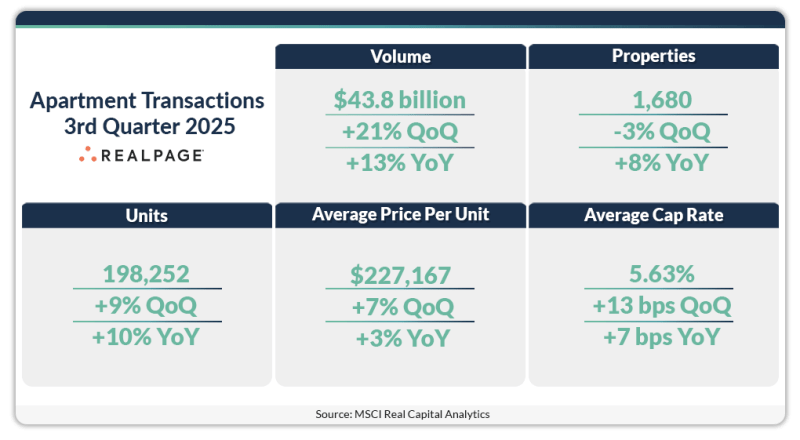

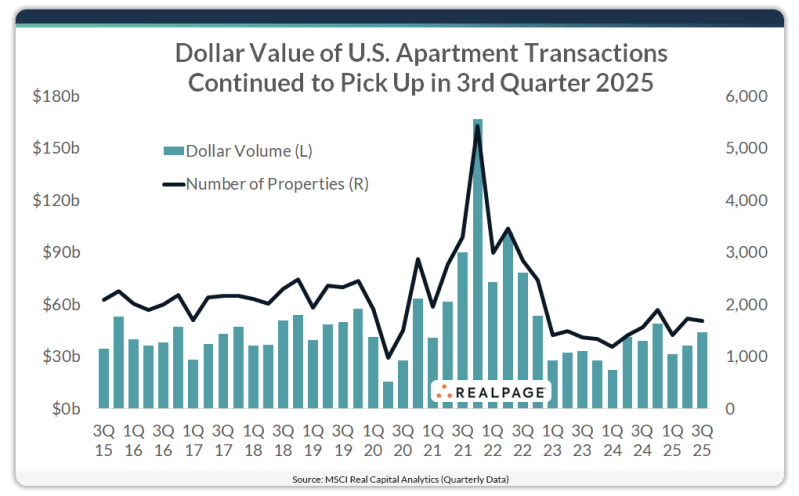

While investment volumes rose, multifamily property valuations did not. The MSCI Commercial Property Price Index showed multifamily as the only major sector experiencing year-over-year price declines, with values down 0.8 percent in September 2025 compared to the previous year. The index was down 19 percent from its 2022 peak.

The number of properties trading hands declined in the 3rd quarter, however, on an annual basis, both the dollar volume and number of properties trading were up.

The average price per unit was $227,167 in 3rd quarter. The per unit pricing averaged about $151,000 from 2015 to 2019.

Cap rates for apartment transactions occurring in 3rd quarter 2025 averaged 5.63%, the highest cap rate in more than eight years and well above the pandemic-era low of 4.65% from 2nd quarter 2022.

The share of first-time home buyers dropped to a record low of 21%, while the typical age of first-time buyers climbed to an all-time high of 40. The share of first-time buyers in the market has contracted by 50% since 2007.

Major apartment REITs reported a shortage of new leases and stagnant rent growth, with some owners going so far as to lower guidance for the remainder of the year as economic concerns grow.

Renewed leases remain steadier as people stay put in uncertain economic conditions, but a dearth of new leases is stifling rent growth, according to third-quarter results released by five multifamily REITs this week.

“Blends began the quarter ahead of our expectations but over the last 45 days have decelerated beyond typical seasonality, which we largely attribute to the economic uncertainty,” said UDR CEO Michael Lacy.

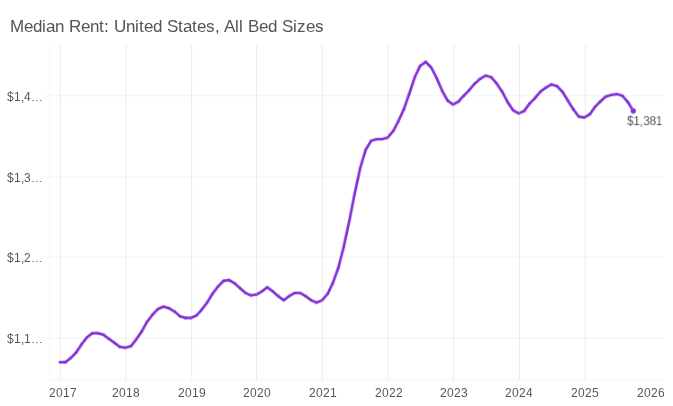

The national median rent fell by 0.8% in October. This was the third consecutive month-over-month decline, as we’re now in the midst of the rental market’s off-season. It’s likely that we’ll continue to see further modest rent declines to close out the year.

Rent prices nationally are down 0.9% compared to one year ago. Year-over-year rent growth has been slightly negative for over two full years, and the national median rent has now fallen from its 2022 peak by a total of 4.2%.

While it’s expected to see rent prices dip slightly at this time of year, there’s been some shifts to the timing of rental market seasonality in recent years. Monthly rent growth peaked at +0.7 percent in March this year, but it then began to gradually trend down during the peak moving months, when rent growth is normally fastest. The flip to negative month-over-month growth also came a bit earlier than pre-pandemic years, making this the third straight year that prices have begun to dip in August.

The national multifamily vacancy rose to 7.2%, setting a new record high for the index. A healthy supply of new units are hitting the market and colliding with sluggish demand, causing vacancies to continue trending up.