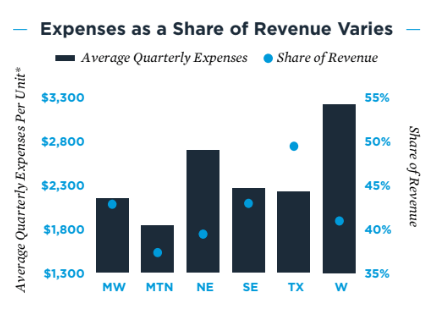

Expenses per unit, and as a percentage of revenue, vary dramatically based on the part of the country (Midwest, Mountain, Northeast, Southeast, Texas or the West) you’re in:

Source: IPA

Expenses per unit, and as a percentage of revenue, vary dramatically based on the part of the country (Midwest, Mountain, Northeast, Southeast, Texas or the West) you’re in:

Source: IPA

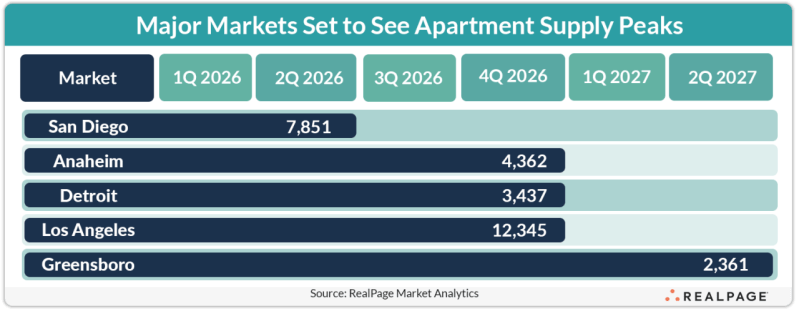

Most major markets are past the point of peak new multifamily supply. Most others will be there at some point this year. Greensboro, NC is scheduled to see supply hit its high point in the second quarter of 2027, when over 2,300 units are slated to complete.

Source: RealPage

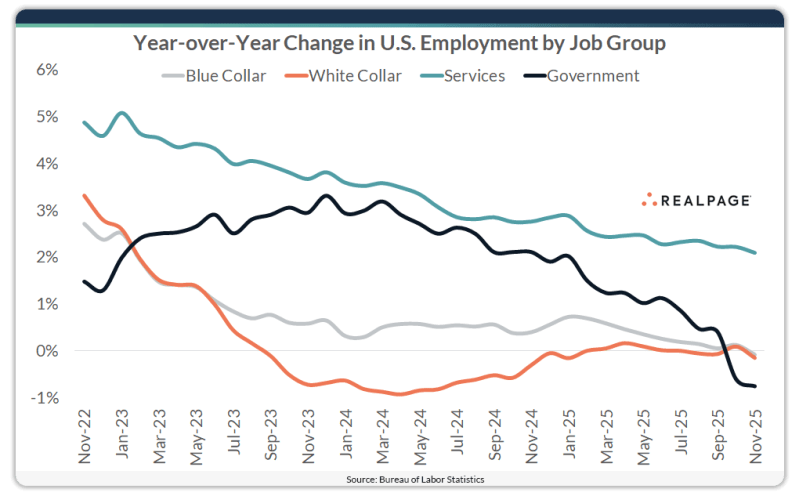

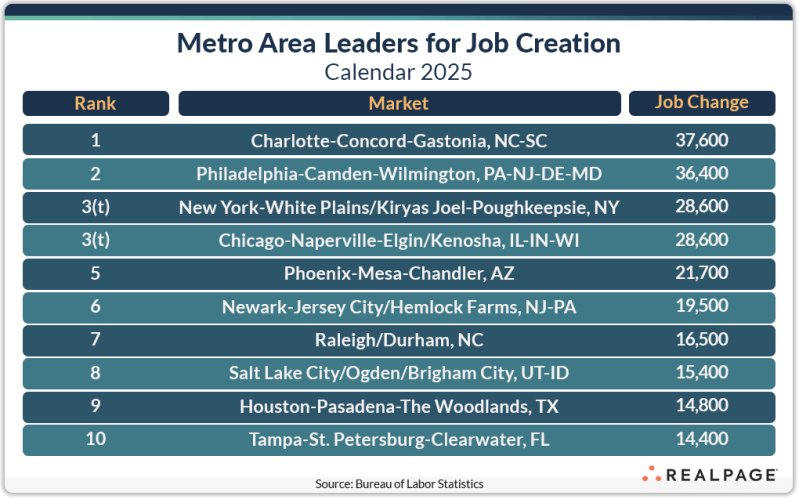

Employment trends across the U.S. showed a clear loss of momentum to end 2025.

Source: RealPage

The Charlotte metro area led the country for job gains for 2025 with 37,600 new jobs created for the year. That was an improvement of 21,800 jobs from 2024’s total.

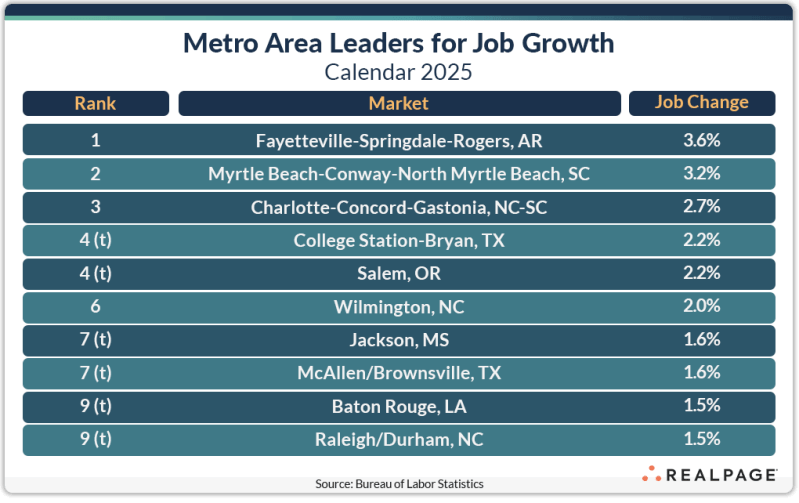

Unlike the top job gain markets, which tend to be large in population and employment, smaller markets usually dominate the top markets for annual percentage change in employment.

Source: RealPage

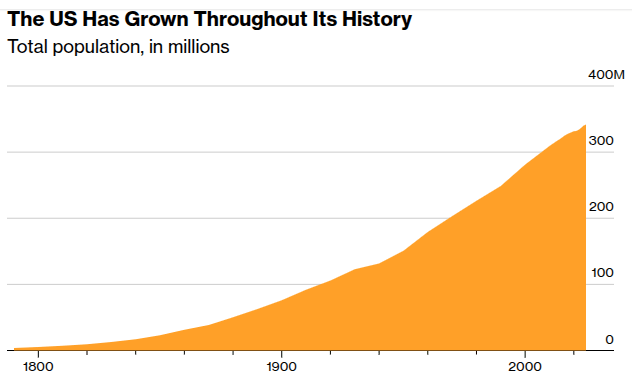

When the US Census last issued long-run forecasts for the population, the main prediction was that it would decline for the first time in 2081. Based on a sharp reduction in new births and net migration, it could now happen as early as 2026.

In the year prior to July 1, 2025 the population grew by only 0.5%, or 1.8 million people, its lowest growth since the pandemic. There were 519,000 more births than deaths, however, by 2030 that surplus is likely to disappear altogether, making the US entirely dependent on immigration for population growth.

Net migration is expected to fall to only 316,000 in the year prior to July 2026, with the US “trending toward negative net migration.” What complicates the picture is that the Census estimates start and end midyear, and with Trump’s policy moving quickly, the official data isn’t keeping up. The Census calculations released this week don’t include the second half of 2025, when the immigration crackdown accelerated.

Recent work by the center-right American Enterprise Institute and center-left Brookings Institution suggests the US is already experiencing net negative migration. Diving into the data available on inflows and outflows of both legal and undocumented foreign-born workers, they calculated the US had a net decline in the immigrant population of 10,000 to 295,000 in 2025.

The biggest contributor to the slowdown in net migration has been a reduction in new arrivals rather than the high-profile deportations now receiving media attention.

If the low end of their 2026 prediction comes true and birth rates don’t spike in an unprecedented way, the US would have a decline of more than 400,000 in its overall population. Even at the midrange of their forecast, the country is at least flirting with a population decline.

Since the US began taking censuses in 1790, such a decline has never been recorded. The only potential asterisk was 1918, when the domestic US population shrank slightly as a consequence of the Spanish flu and because some 2 million US soldiers were deployed abroad.

Source: Bloomberg

Shelter makes up about 33% of the Consumer Price Index (CPI), which is the most popular gauge of inflation.

The shelter component of CPI has remained stubbornly high for multiple reasons. It looks at the data on a significant lag, and a large component of the data collection is just calling people up and asking them what they think their home would rent for.

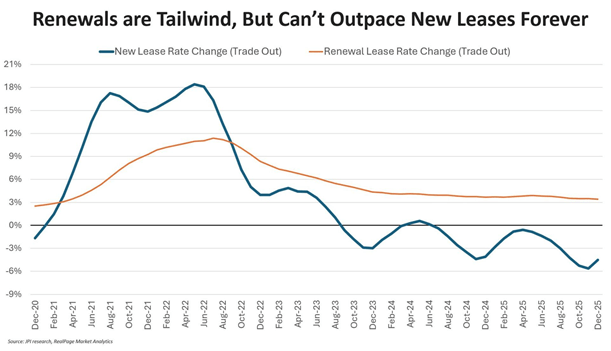

A less discussed reason is that while new rents have been falling in some markets, renewal rent growth has remained above 3%. Renewal rents make up about two thirds of all leases, depending on the market.

Source: Gavin Campbell

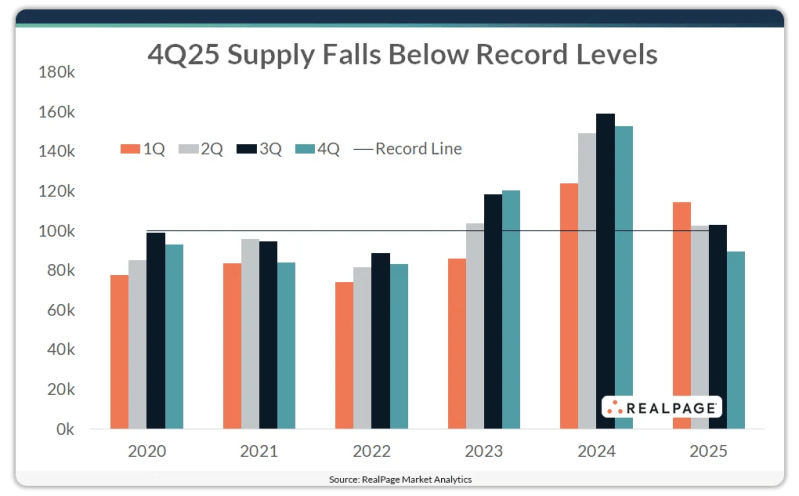

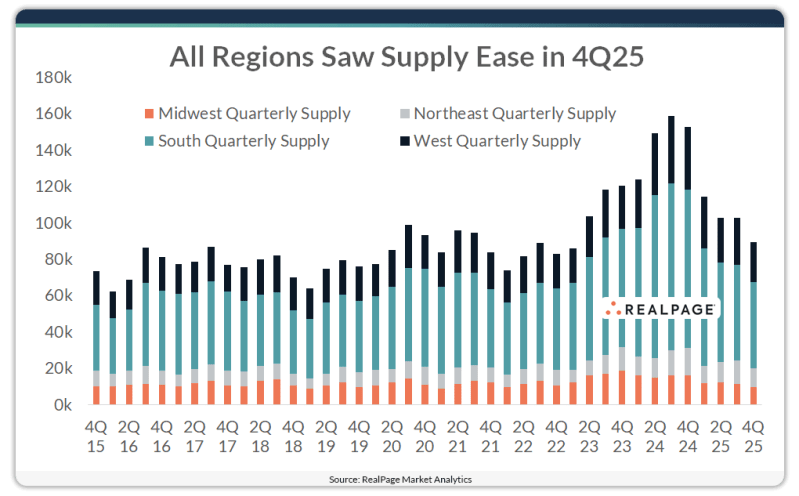

Roughly 89,400 units wrapped up construction in 4th quarter 2025, marking the first time in 11 quarters that deliveries fell below the 100,000-unit mark.

All regions of the U.S. saw supply volumes ease in 4th quarter, however, the South has also seen the steepest pullback in delivery volumes recently. Completions in the South peaked at nearly 91,800 units in 3rd quarter 2024 and volumes have fallen off every quarter since. The last three months of 2025 marked the first time South region completions totaled less than 50,000 units in 11 quarters.

Source: RealPage

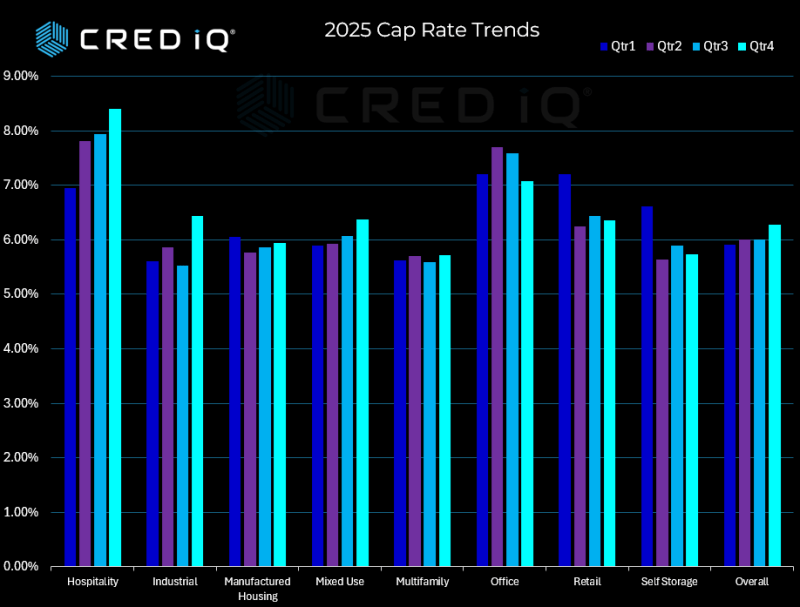

“Commercial real estate cap rates exhibited a steady upward trajectory throughout 2025, according to CRED iQ’s comprehensive loan analytics, with overall market cap rates expanding from 5.91% in Q1 to 6.28% by year-end.

Multifamily properties demonstrated remarkable resilience, maintaining the tightest cap rate band among major property types. Starting at 5.63% in Q1 and finishing at 5.71% in Q4, multifamily’s mere 8-basis-point expansion reflects sustained investor confidence in residential fundamentals and the asset class’s defensive characteristics.”

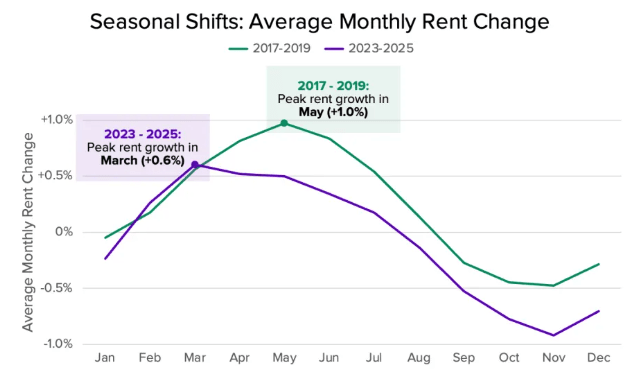

The rental market tends to follow an established seasonal pattern. More people generally move during the spring and summer, and rent prices normally rise accordingly as multifamily operators increase rents in response to the spike in demand. During the fall and winter months we tend to see the opposite: less moving activity, and operators pulling back on rents to attract the dwindling set of renters still on the market for a new home.

This seasonality results from three practical factors: school, weather, and holidays. The summer is more favorable for all three: if you are a student or have young children, you don’t need to juggle school schedules; weather is generally more temperate; and moving expenses aren’t being eaten up by holiday spending. Renters who have the flexibility and means to relocate during the winter will generally find lower prices and more wiggle room for negotiating lease terms.

Over the past three years, we’ve seen a noticeable shift in the timing of this seasonality. Since 2022, rental activity is more evenly distributed throughout the calendar year, annual rent declines exceed annual rent increases, and peak rent growth has moved up earlier in the year.

From 2017-2019, the typical seasonal pattern was this: nationwide rents would rise for seven months from February through August, with peak rent growth (+1.0 percent) occurring in May.

Since 2023, there has only been six months of rent growth each year, from February through July, with peak rent growth down to +0.6% and occurring two months earlier in March.

These shifts are due to a combination of factors including:

Source: ApartmentList

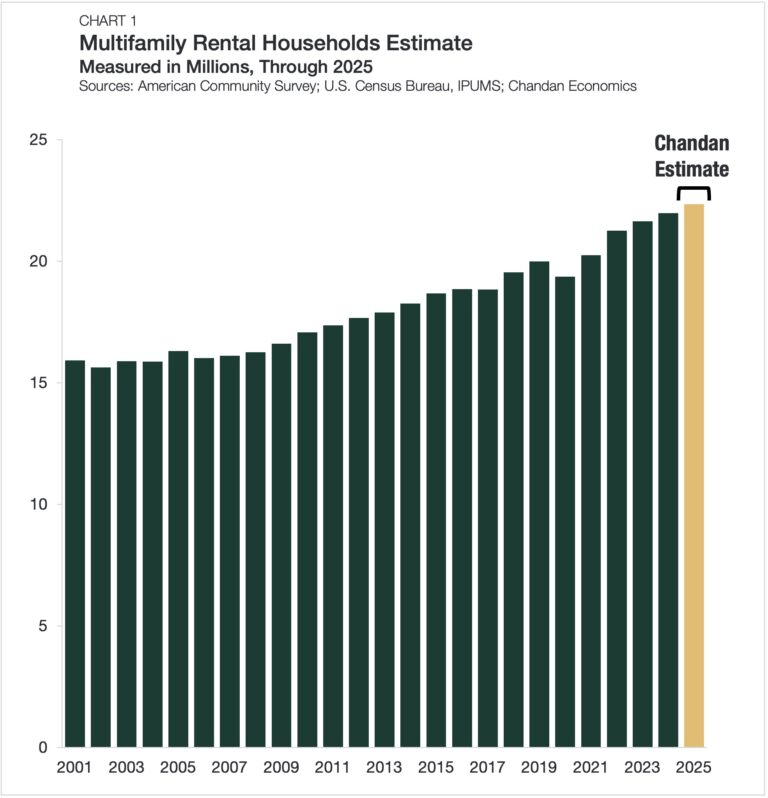

The multifamily rental households estimate reached an all-time high of 22.4 million in 2025. Annual growth rate remaining between 1.6% and 1.8% in each of the past three years. The net gain of 3.0 million multifamily households since 2020 is the most for a five-year period in more than 20 years.

Source: Arbor