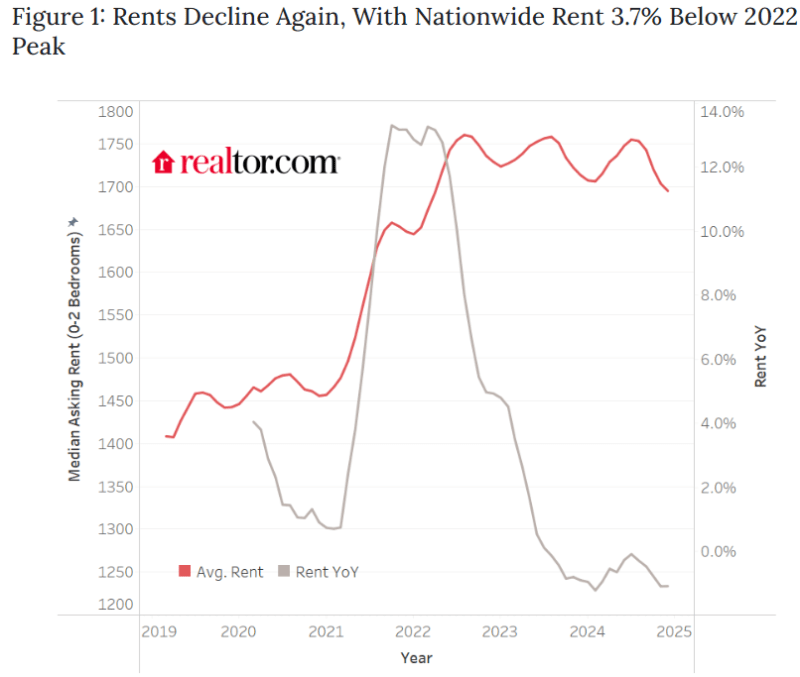

From the Wall Street Journal: “We’re Heading Toward a Landlord-Friendly Era. Expect Higher Rent Prices“

- More people now are renting longer, as mortgage rates stay high and the costs of homeownership remain unaffordable for many Americans. Landlords say that the new construction pipeline should be mostly drained by year-end, setting the stage for rents to rise nationwide later this year.

- The relationship is going to very quickly flip from a renter-friendly environment to a landlord-friendly environment,” said Lee Everett, the head of research and strategy at multifamily giant Cortland.

- By the end of this year, every major metropolitan market is expected to see positive rent growth, said Jay Lybik, national director of multifamily analytics at CoStar.

- More tenants are in heated battles for vacant space. Last year, an average of nine prospective renters were competing for every open apartment unit on the market, according to Rent Cafe.

- Apartment absorption, a metric of rental demand that measures the change in how many units are leased, was higher last quarter than any other fourth quarter since at least 1985, according to real estate firm CBRE.

- Apartment investors are placing bets on the Sunbelt’s 2025 rebound. Equity Residential, a publicly traded multifamily landlord, paid more than $274 million in the fourth quarter for three properties in Atlanta and Denver.

- Some investors that previously exited the Sunbelt market are returning. After selling all of its Sunbelt properties three years ago, Gaia Real Estate, a national real-estate investment and management firm, told The Wall Street Journal that it launched a new Sunbelt-specific acquisition arm with Raymond James as its investment bank. The new REIT has already bought three Sunbelt properties. “We assume that the second half of 2025 [into] 2026 will be back to rent growth,” said Gaia CEO Danny Fishman. “We are playing the wave.”

______________________________________

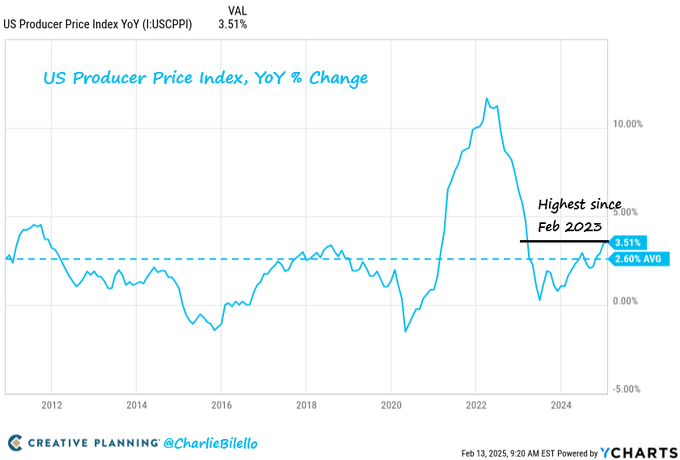

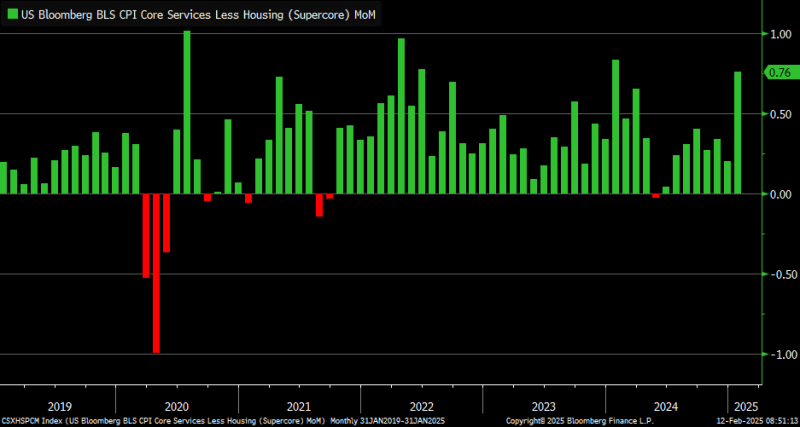

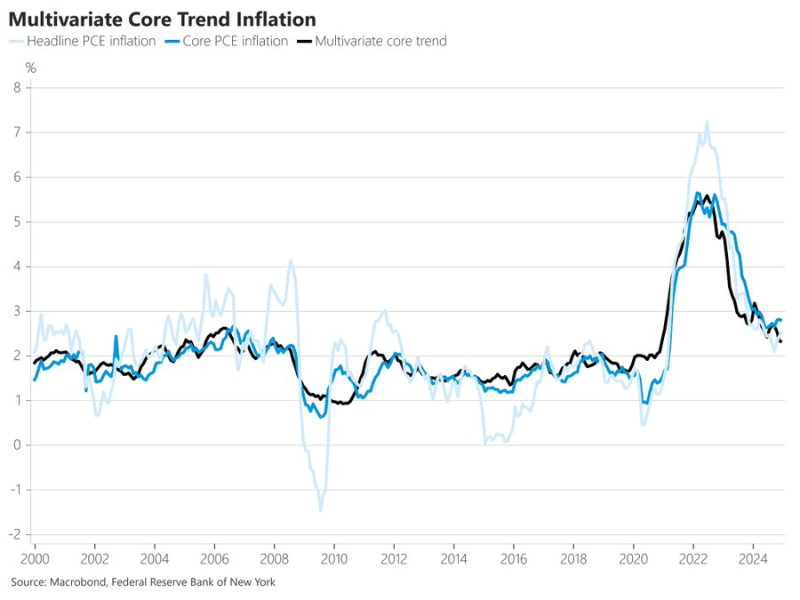

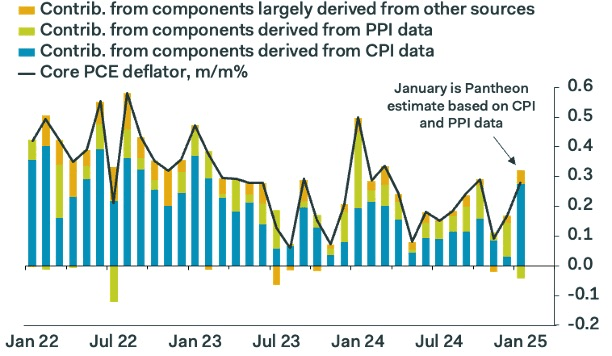

The PPI numbers were a game-changer for the Core PCE print coming at the end of the month (Core PCE is the inflation gauge the Fed believes is most important). We’re now tracking 0.28% month-over-month, 2.6% year-over-year (down from 2.8% in December) All the healthcare and insurance PPI components were weak and airline fares prices fell sharply. About as good as the Fed could have hoped for.

__________________________________________

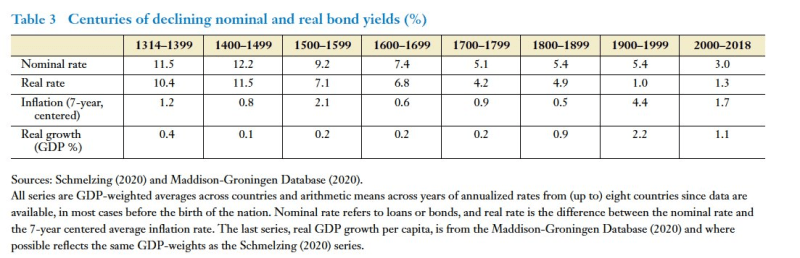

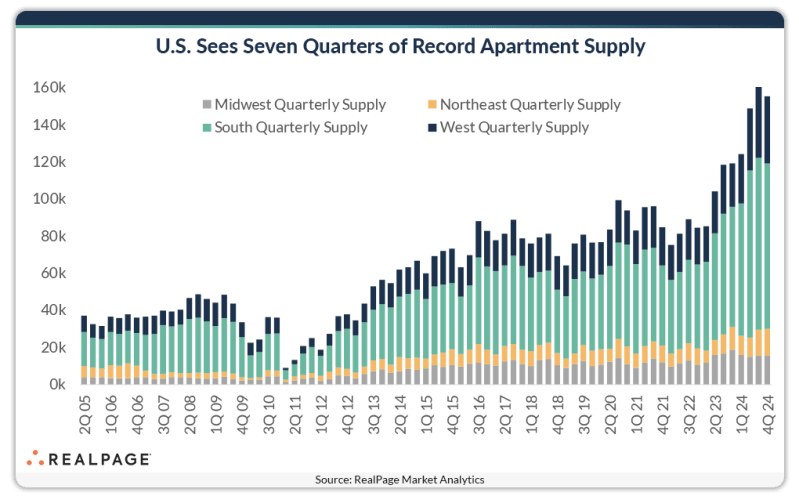

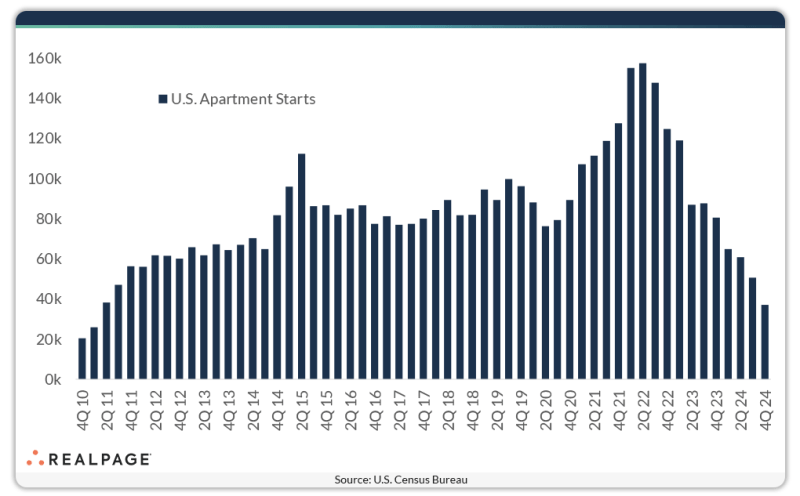

Multifamily Starts Hit Lowest Since 2011:

U.S. multifamily starts have declined precipitously in the past year and a half and hit a 13-year low mark in 4th quarter 2024. A little over 37,000 apartment units got off the ground in the last three months of the year.

___________________________________________

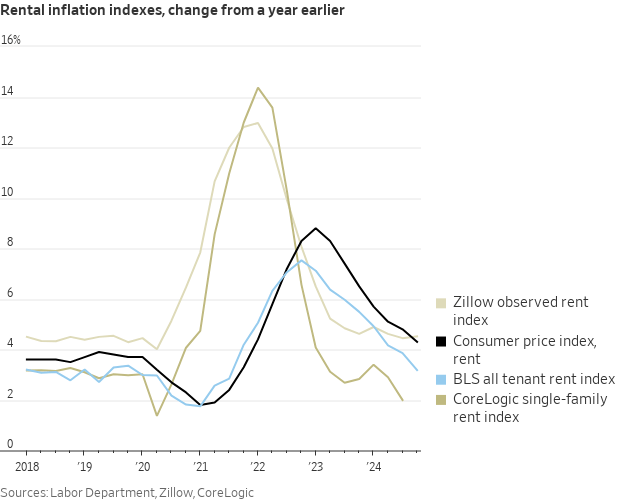

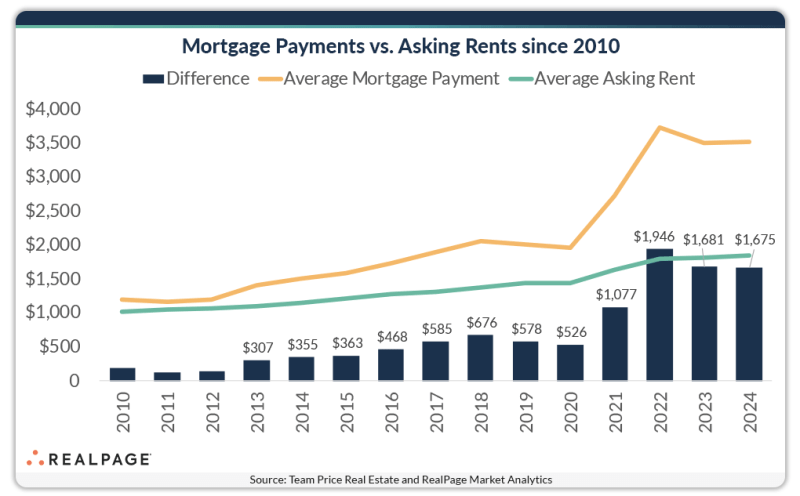

Average hourly earnings in the U.S. grew at an average annual rate of 3.1% between 2010 and 2024. However, during the same time period, the median price of an existing single-family home rose much faster at an average annual rate of 6.7%, more than double the pace of wage growth. By the end of 2024, the median home price had reached approximately $418,000, nearly doubling from $212,000 in 2014.

Rental affordability has followed a different trajectory. The median rent-to-income ratio stood at 22.2% at the end of 2019, peaked at 23.8% in 2021, and then declined to 23.3% by the end of 2023. By the end of 2024, it had settled at 22.5%, just 30 basis points above pre-pandemic levels. This suggests that as inflation has cooled, wages have grown steadily and rents have stagnated over the past few quarters, making renting nearly as affordable as it was before the pandemic, with some variation across markets. In contrast, homeownership has not seen the same affordability improvements, as home prices remain significantly higher relative to income growth.

______________________________________

Fannie Mae’s 2025 Multifamily Outlook: Clearer Skies Ahead

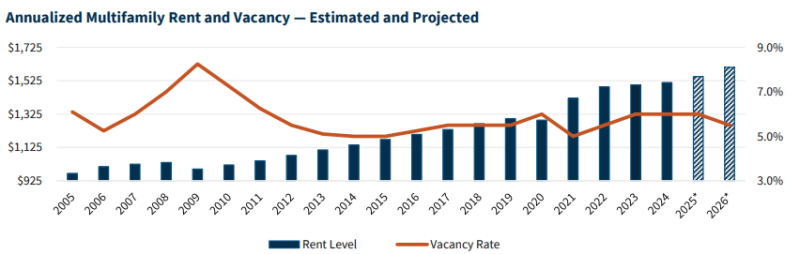

We have upgraded our outlook for the national multifamily sector to “improving” for 2025. We expect the multifamily sector will see slow but continued improvement in demand this year, possibly resulting in flat rent growth and a slightly rising national vacancy rate during the first quarter of 2025 due to the amount of new supply entering the market, especially during what is normally a slow lease-up time of year. After that period, we expect multifamily fundamentals will strengthen, with moderately increasing rent growth and stabilizing vacancy levels.

We anticipate that cap rates are likely to compress a bit more during 2025, likely declining to between 5.0% and 5.5% over the next 12 to 18 months, helping to spur more sales transaction volume over that time.

At a national level, we believe that demand for multifamily rental will increase slightly in 2025, based on expected job growth and household formations as well as demographic trends. As of 2022, there were an estimated 68 million people between the ages of 20 and 34 years old, which is the cohort most likely to rent a multifamily unit. The U.S. Census Bureau estimates that this cohort could increase by nearly 1.0% by 2032 — meaning an increase of more than 670,000 people in this age cohort in just a decade. This growth is one key reason we expect demand for

multifamily rental to continue over the long term. In the short term, a rise in new jobs is the other reason. Year-over-year job growth is expected to remain positive through at least 2026, according to Fannie Mae’s latest economic forecast. We expect the economy will add an estimated 4.5 million new jobs between 2024 and 2026. This should help keep new multifamily rental demand steady over the next few years.

Although there are currently more than 632,000 multifamily rental units slated for completion in 2025, we believe it is very unlikely that all those units will be completed before year end, due primarily to ongoing labor shortages and construction delays, notably permitting delays.

_______________________________________

From Cushman & Wakefield’s Quarterly Market Report:

2024 was a banner year for multifamily absorption. More than 436,000 units were absorbed – a 72% increase over 2023 and 56% above the 2017-2019 average. Every one of the 90 markets tracked by Cushman & Wakefield Research posted more net move-ins than move outs, with the Sun Belt continuing to lead in growth.

Construction risk is quickly diminishing. Construction activity has fallen 40% from its peak, with new starts down to just 230,000—the lowest level since 2012. High interest rates, weaker effective rent growth, and rising replacement costs continue to hinder new development. Most apartments slated for delivery by 2028 have already broken ground, setting the stage for a tighter supply environment over the next three to four years.

_________________________________________

From Colliers’ Quarterly Market Report:

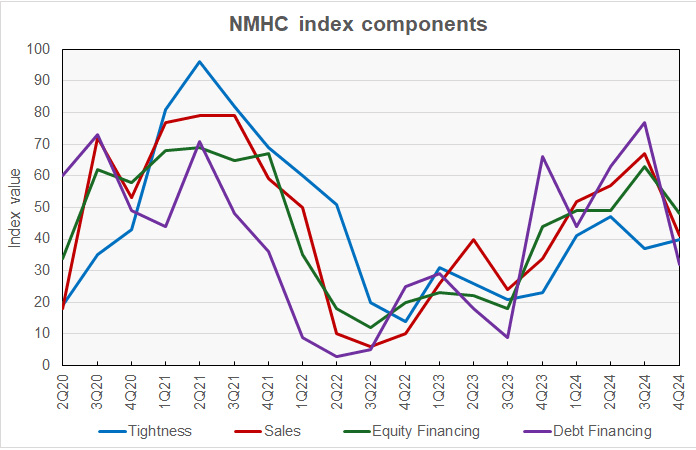

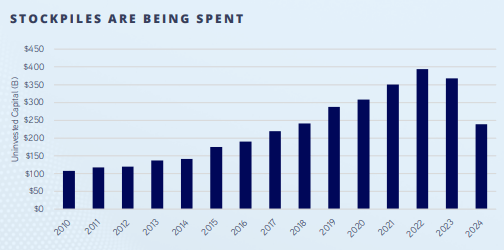

Investors are coming back to the multifamily market with a vengeance. Volume increased by a healthy 22% in 2024, leading all asset classes. Consistent monthly activity indicates the market has turned a corner. Investors are intrigued by the confluence of peaking supply-side pressure, limited new groundbreakings due to elevated borrowing costs, and the high cost of homeownership, keeping renters renewing at historically high levels. This results in a path to rent growth in the quarters ahead. Additionally, many deals are being done below replacement costs, and capital is coming off the sidelines.

Investors are deploying their capital stockpiles, and there is no reason to suggest that multifamily won’t receive its fair share. Timing is important, and with signs of brighter days ahead, expect investors to continue chasing multifamily assets in 2025.

_____________________________________________