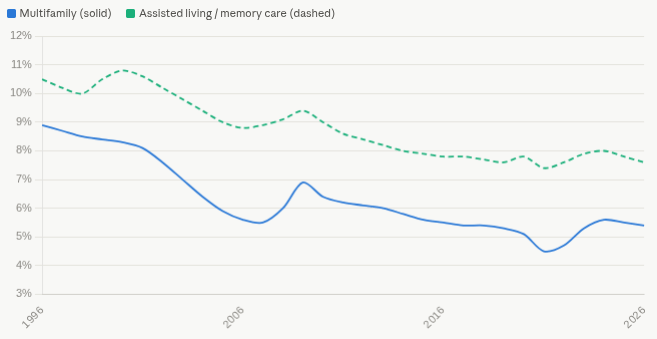

Assisted Living and Memory Care properties have always traded with a cap rate spread above multifamily. Why?

Operating Business Risk

- An apartment is a passive real estate asset; assisted living/memory care is a healthcare-adjacent operating business inside real estate. Buyers underwrite the operator as much as the building, and NOI can swing dramatically based on management quality.

- Operator dependence creates transition risk — replacing an underperforming operator is far more disruptive than swapping property managers on an apartment deal.

Labor Intensity

- Labor runs roughly 55-65% of operating expenses in AL (higher in memory care) versus ~25-30% for multifamily, so wage inflation, caregiver turnover, agency staffing costs, and staffing regulations hit NOI directly.

- The caregiver labor pool is structurally tight, and owners have limited ability to control that cost line.

Resident Turnover Economics

- Average length of stay is only 18-28 months in AL and roughly 18 months in memory care, versus 2-3 years for apartment tenants — meaning 40-60% of the rent roll must be re-leased every year just to hold occupancy flat.

- Move-outs are driven by health decline or death rather than lease expirations, and move-ins depend on emotionally difficult family decisions, making census harder to predict and market.

Regulatory and Licensing Exposure

- Communities are state-licensed and subject to surveys and inspections; a deficiency citation can damage reputation and census in ways multifamily never faces.

- Regulations (staffing ratios, care requirements) can change and compress margins with no offsetting revenue.

Liability and Litigation Risk

- Resident acuity creates negligence and wrongful-death exposure, especially in memory care, driving higher insurance costs and legal risk.

Thinner Capital Markets

- The buyer pool is smaller and more specialized than multifamily’s, reducing exit liquidity.

- Debt is less abundant — multifamily enjoys deep, consistent GSE support, while senior housing financing is narrower and more sensitive to credit cycles.

Higher Expense Loads and Margin Sensitivity

- Food service, care staff, transportation, and activities create a heavier expense structure, so a small revenue miss translates into a larger NOI miss than in multifamily.

Segment Risk Premium Scales with Care Level

- The market prices this explicitly: active adult trades nearly on top of multifamily, independent living slightly wider, assisted living wider still, and free-standing memory care widest (~9.5%+) — the more care in the model, the bigger the spread.