Master Planned & Build-To-Rent Communities:

- There’s been a dramatic shift in Master-Planned communities since 2018. Master-planned developers initially resisted rental components, but now nearly all are incorporating them. They’ve discovered that renters often become homebuyers within their communities, providing earlier land sales and better cash flows.

- Build-to-Rent is in the early innings and remains a huge long-term opportunity. With 11-14 million people renting homes compared to 24-30 million apartment renters, the industry should be building around 150,000 rental homes annually (currently falling short). BTR will remain cyclical in the short term (based on the economy), but he views it as a decades-long investment opportunity when you zoom out and look at the bigger picture.

Key Demographic Shifts Shaping Future Demand:

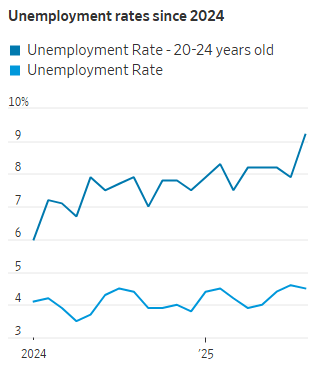

- Essentially zero growth in the 25-34 age group over the next decade. Builders need to rethink standard apartment development projects where they assume college graduates will be there to lease them up.

- Major growth in 45-54 and 75+ populations. While assisted living will benefit, other segments will as well. There are many lifelong renters in the 45-54 age group that appreciate certain types of amenities and apartment styles. A.I. will improve lifespans and health, even for those in the 75+ bracket.

- More young people living alone (boosting one-bedroom demand). People used to always live with other people and never live with their parents. More people are living with their parents, but when they move out more are living alone.

- Fewer divorces and children, changing household formation patterns. People have less need to move up in size to a home if they do not have children.

New Supply and Immigration:

- While new supply has the effect of lowering rents for all properties (class B renters move up to discounted class A units and class C renters move up to discounted class B units), the opposite effect happens with immigrants. They fill class C properties which pushes tenants up to class B, which pushes tenants up to class A, moving rents upward across all properties.

Renting vs. Buying Affordability:

- The gap between the all-in cost of owning a home (mortgage, taxes, insurance, etc) and renting a similar style home at $1,400 per month. The historical gap is closer to $300 per month.

- Burns thinks the Fed’s inflation target is 2.00% and the Fed Funds rate target is 3.50% (150 basis points above the inflation rate). Historically the 10-year treasury is 100 to 140 basis points above the Fed Funds rate, which would be 4.50%. Mortgage rates are typically 150 to 200 basis points above the 10-year treasury which would mean they’re in the low 6% range (which is right about where they are right now).

- That will create a tailwind for the apartment market for many, many, many years because it will remain much more affordable to rent than own for an extended period.

- That means there is going to be continued pressure on home buying affordability, which will continue to be very positive for apartments and build-to-rent communities.

Source: The Rent Roll Podcast