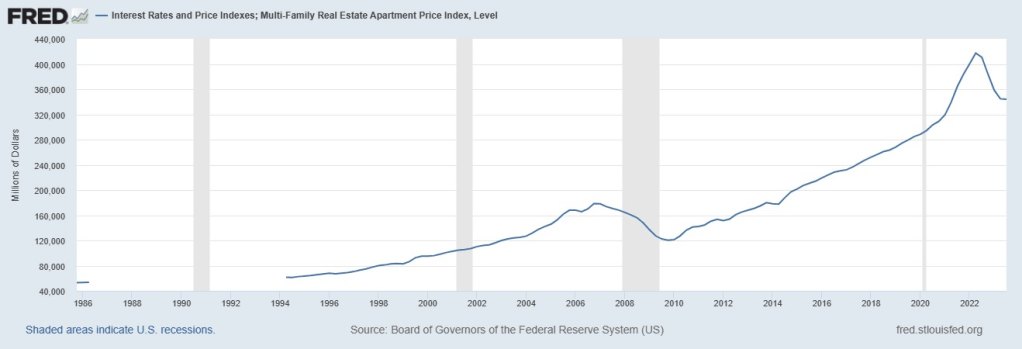

The Federal Reserve released multifamily price data through the end of Q3 showing a 2.1% decline quarter-over-quarter and a 16.2% decline year-over-year.

The Federal Reserve released multifamily price data through the end of Q3 showing a 2.1% decline quarter-over-quarter and a 16.2% decline year-over-year.

Monthly and annual rent changes through November:

| Source: | Month: | Monthly: | Annual: | Vacancy: |

| Apartment List | November | -0.90% | -1.10% | 6.40% |

| CoStar | November | -0.25% | 0.83% | 7.31% |

| Real Page | November | -0.52% | 0.16% | N/A |

| Apartments Advisor | November | -1.83% | -2.83% | N/A |

| Apartments.com | November | -0.30% | 0.80% | N/A |

| Yardi Matrix | November | -0.35% | 0.40% | 5.10% |

| Rent.com | November | -0.57% | -2.09% | N/A |

| Zillow Single Family Homes | November | -0.20% | 3.30% | N/A |

| Zillow Multifamily | November | -0.30% | 2.50% | N/A |

| Redfin | November | -0.60% | -2.10% | N/A |

| Realtor.com | November | -0.69% | -0.60% | N/A |

| Average: | -0.59% | -0.07% | 6.27% |

28% of fall 2024 student housing beds were pre-leased through November. This is a record high, and it was also the largest October to November increase (17%) in history.

Removing the last two years of record demand, beds are usually about 20% pre-leased by the end of November. A handful of schools (Tennessee, Purdue, Clemson, Arkansas and Wisconsin) have already pre-leased about 2/3 of their privately owned student housing beds.

Asking rents for student housing grew 7% year-over-year through November while many multifamily markets across the country have experienced declines.

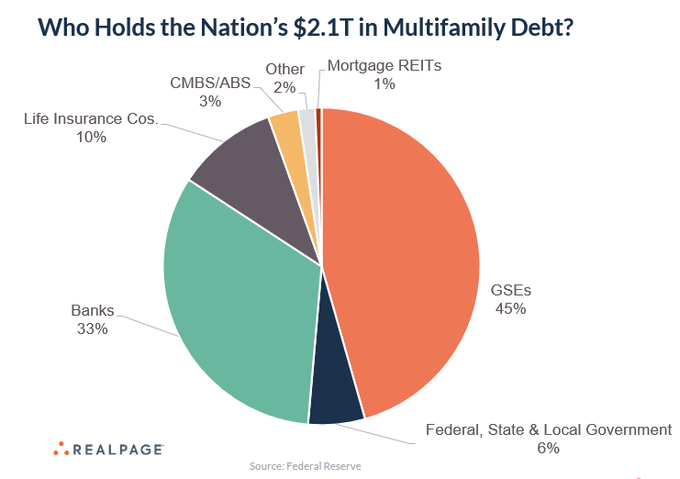

An excellent visual walk-through on interest rates, multifamily debt markets, rate caps and the economy.

Debt funds and CMBS are getting all the headlines for at-risk loans, but together they represent less than 5% of the $2.1 trillion in multifamily debt. The majority of the riskiest bridge loans were concentrated within debt funds, which represent only $42 billion of the total pie.

Delinquency rates at banks (0.40%), Freddie Mac (0.29%) and Fannie Mae (0.54%) remain extremely low (so far).

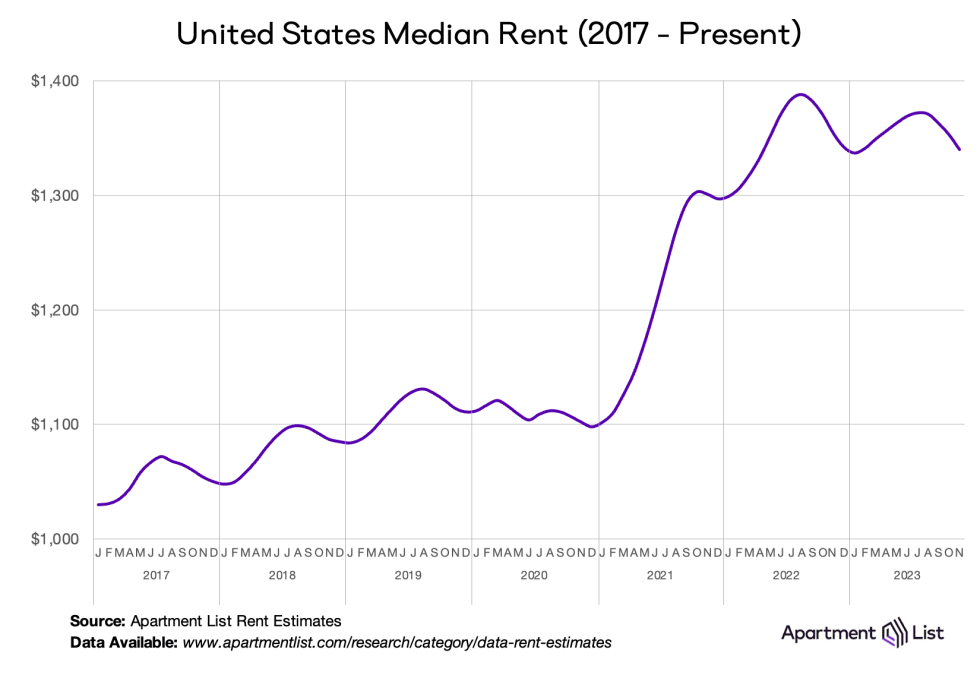

U.S. rents are still digesting the incredible rise during 2021 and the first half of 2022. Rents are below their peak in many markets across the country and continue to fall month-over-month, especially when concessions are taken into account.

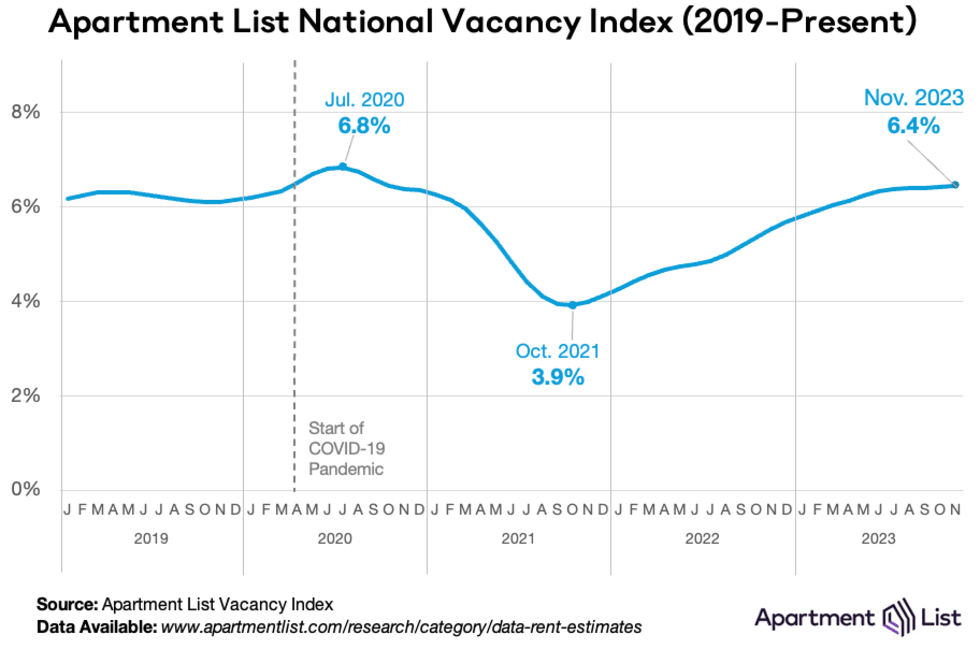

Vacancy rates are back to pre-pandemic levels:

One million apartments are currently under construction with new deliveries set to surge throughout 2024 before starting to decline in the second quarter of 2025:

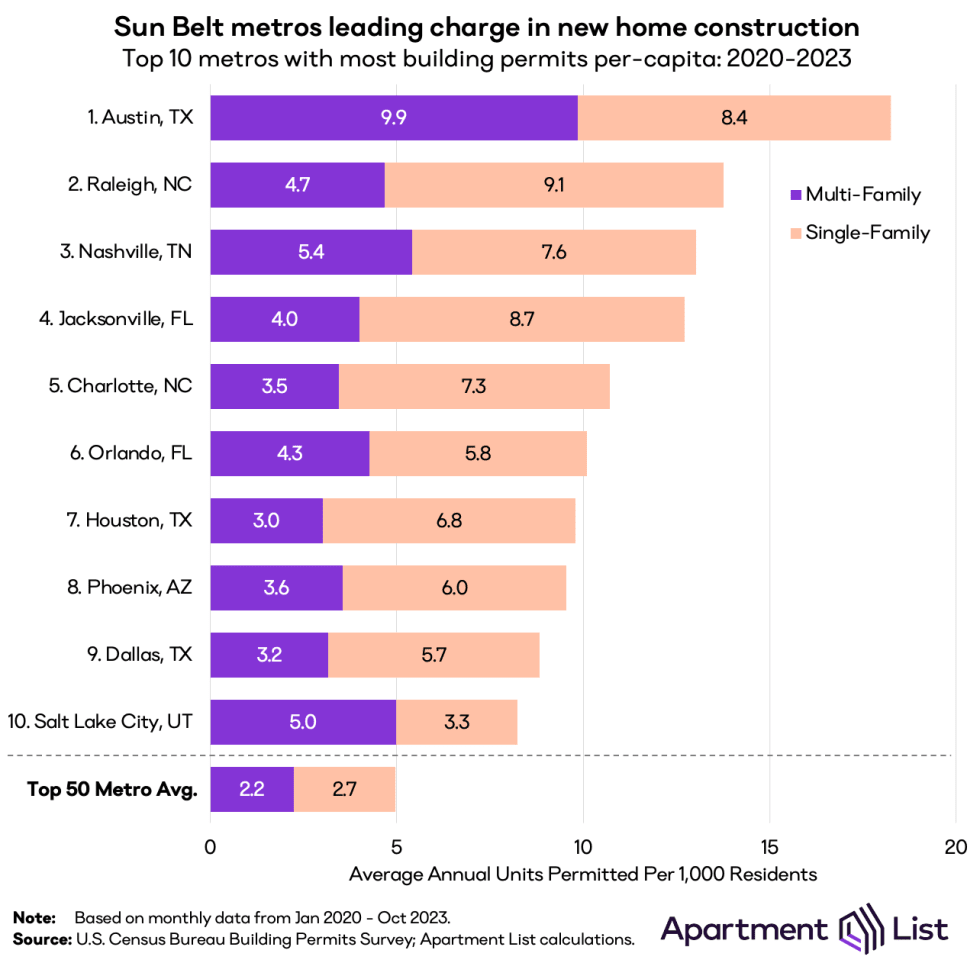

The sun belt is faced with an enormous supply surge. These are high population growth markets, but they have experienced some of the largest rent declines in the country over the last year.

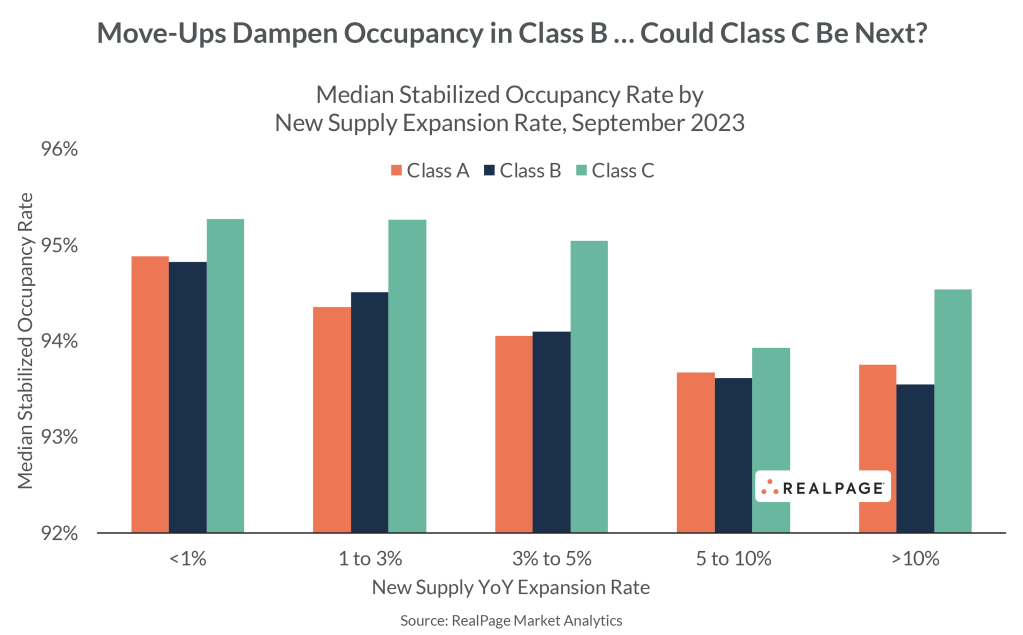

Multifamily REIT CEOs have been commenting on earnings calls that the concessions (1 to 3 months of free rent) from class A buildings are now putting downward pressure on their class B property rents. This is not something they were experiencing in the first half of 2023. Many renters can now afford to move up to a class A community with these concessions in place (3 months of free rent is equivalent to a 25% drop in rents).

When the 10-year treasury hit 5% in October, builders suddenly felt pressure to hit 90% occupancy by year end to try and sell or put permanent financing on their buildings. This is creating a fire sale with rent concessions.

The greater the percentage of new supply relative to the current inventory of apartments in a city, the larger the impact on class B and C properties:

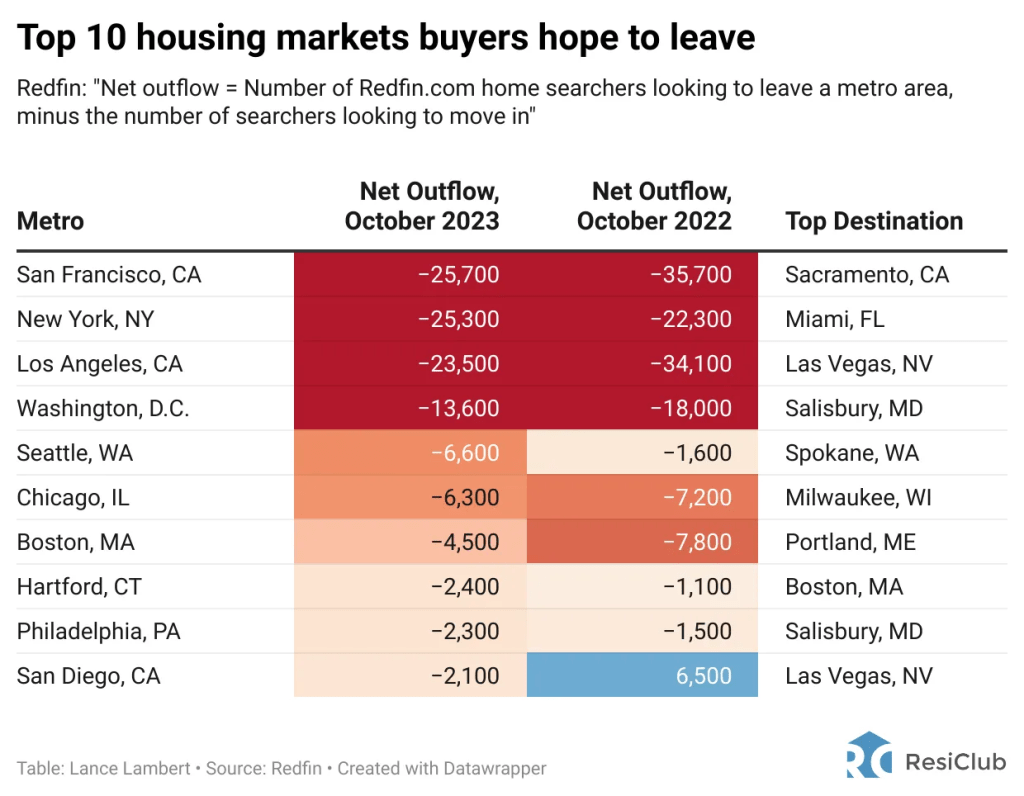

The general trend continues with buyers hoping to leave higher price markets in the northeast and California:

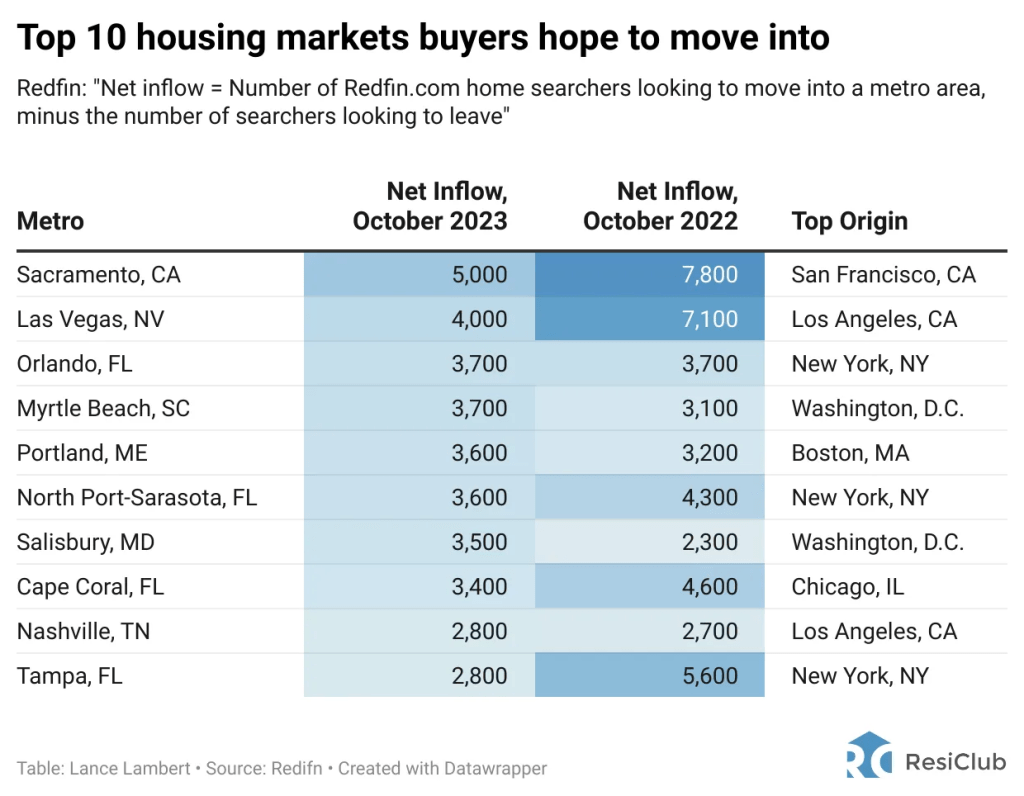

And move to less expensive and warmer regions of the country:

Monthly and annual price changes through October:

| Data Source: | Data Month: | MOM Change: | Annual Change | Data Release: |

| Green Street | Oct 2023 | -8.60% | -14.00% | November |

| MSCI | Oct 2023 | -1.00% | -12.60% | November |

| Average: | -4.80% | -13.30% |

Monthly and annual rent changes through October:

| Source: | Month: | Monthly Change: | Annual Change: | Vacancy: | Data Release: |

| Apartment List | Oct | -0.70% | -1.20% | 6.40% | 10.30.23 |

| Apartments Advisor | Oct | -0.52% | -0.48% | N/A | 11.1.23 |

| CoStar | Oct | -0.47% | 0.74% | 7.15% | 11.1.23 |

| Apartments.com | Oct | -0.40% | 0.70% | N/A | 11.7.23 |

| Redfin | Oct | -1.60% | -0.30% | N/A | 11.8.23 |

| Zillow | Oct | -0.10% | 3.20% | N/A | 11.8.23 |

| Yardi Matrix | Oct | -0.20% | -0.40% | 5.10% | 11.16.23 |

| Rent.com | Oct | -1.64% | -0.29% | N/A | 11.20.23 |

| Realtor.com | Oct | -1.03% | -0.35% | N/A | 11.28.23 |

| Average: | -0.74% | 0.18% | 6.22% |