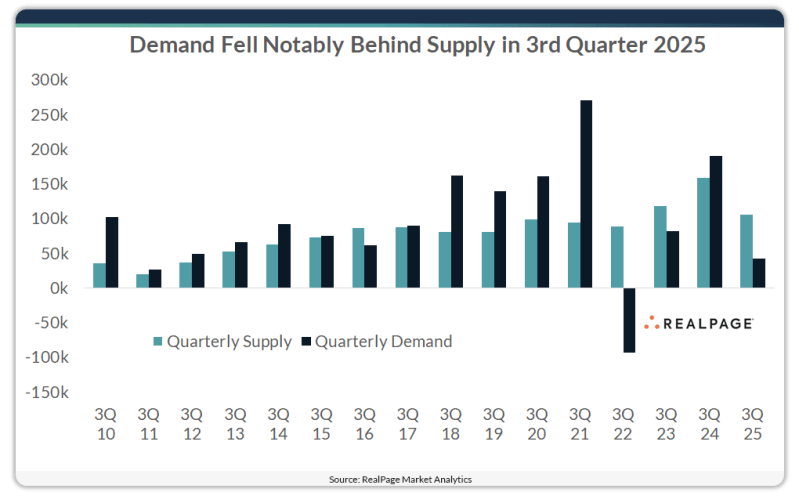

U.S. apartment demand slowed in 3rd quarter, coming in well behind concurrent supply volumes. A little over 42,430 market-rate units were absorbed in the July to September time frame. This performance was about half the decade average for the market and quite a slowdown from what the U.S. has seen in much of the past two years.

This pullback seems to be driven largely by softening employment numbers, gloomy consumer sentiment and general uncertainty in the economy. Supply in 3rd quarter was also lower than what the market has seen in recent years, as the U.S. comes down from the delivery mountain that peaked in 2024. Still, at 105,525 units, supply for the quarter was still well ahead of concurrent demand.

Demand landed nearly 63,100 units short of concurrent supply in 2025’s 3rd quarter, marking one of the nation’s deepest 3rd quarter disparities going back to 1993. Only 3rd quarter 2022 saw demand fall further behind supply, and that was the result of the deep net move-outs during the quarter.

Renters across much of the U.S. have enjoyed easing prices and months of free rent this year. Now, this tenant-friendly environment looks poised to extend deep into next year, and perhaps beyond.

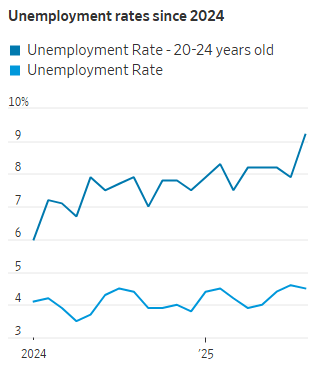

Apartment rents nationally are advancing at their slowest pace in years, thanks to the glut of new units that has taken longer than expected to absorb. More recently, job concerns among young people are posing a new threat to the rental market.

The U.S. unemployment rate for people aged 20 to 24 was 9.2% in August, more than double the overall rate. If a weaker job market continues, it could lead more of these renters to seek roommates or move back with their family, rather than get their own place.

National rent prices edged slightly higher for part of this year, buoyed by price rises in the Northeast and Midwest where new supply has been limited. But last month, national average rent fell 0.3% from August, the steepest September drop in more than 15 years.

Multifamily owners and analysts anticipated that 2025 would be the year that surplus supply balanced out and they regained their pricing power. Instead, landlords are now betting on the ability to raise rents by the end of 2026, or at least sometime in 2027.

Even that might be wishful thinking. Yardi Matrix recently lowered their projections for 2027 rent growth. They expect “more tepid” growth that year because of more new apartments coming online than originally expected.

Previously reliable demand drivers are starting to fizzle. Hiring for entry-level jobs is tightening. Employment growth is decelerating. Apartments are getting leased at record levels. But that is largely because of all the supply and because building owners are offering more tenant incentives. They agreed to concessions such as months of free rent on 37% of rentals in September—a record for that month—according to Zillow.

Some of the signs emerged this summer. Typically the hottest leasing season of the year, when college graduates start new jobs and rent new apartments, this summer saw national rent growth cool even further.

Softening fundamentals in the U.S. apartment market resulted in effective asking rents falling 0.3% in 3rd quarter. This was the first time rents have been cut between July and September since 2009, at the end of the Great Financial Crisis. In the year-ending 3rd quarter, rents were down a mild 0.1%.

Nearly 22% of apartments were offering concessions as of 3rd quarter, and the average concession was 6.2%. As operators focus on filling units in the coming months, concession utilization could become even more prevalent, making true rent growth harder to realize until discounts burn off.

Newmark shows their estimated size of the “potentially troubled” multifamily loans by year in the graph below. While $81 billion sounds like a lot, it’s less than 5% of the total multifamily debt market, and most of this stack will continue to get pushed forward into the future with lenders and property owners hoping interest rates come down or their NOI improves (or both).

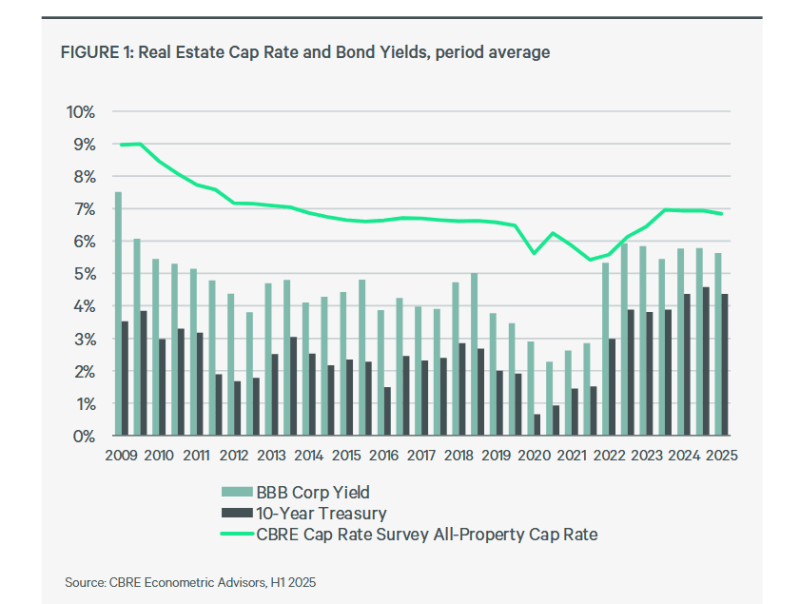

Most graphs show commercial real estate cap rates in relation to the 10-year treasury, but the graph below adds investment grade corporate bond yields.

Why the two do not interact the same way cap rates and the 10-year treasury do, it is instructive to see what investors are paying relative to other risk assets.

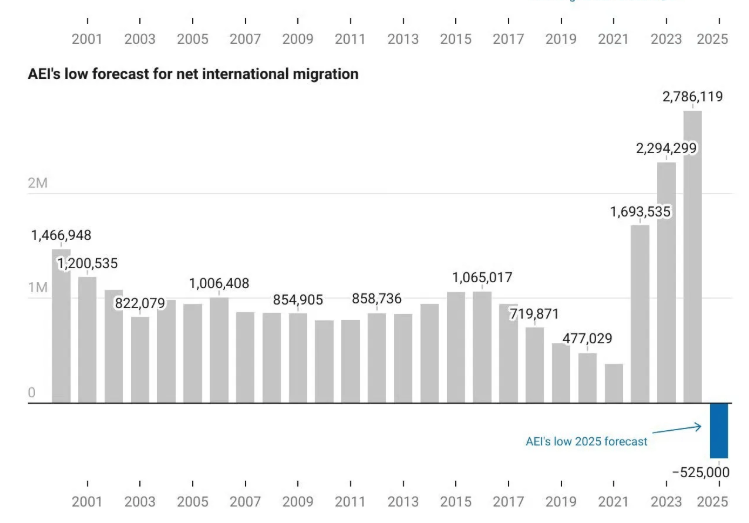

For nearly 250 years, America has only known growth. 2025 could be the first year on record the US population shrinks. Population growth has two sources:

Natural increase (births minus deaths)

Net immigration (arrivals minus departures)

Last year, births outnumbered deaths by 519,000, and AEI estimates that net migration in 2025 could be negative 525,000.

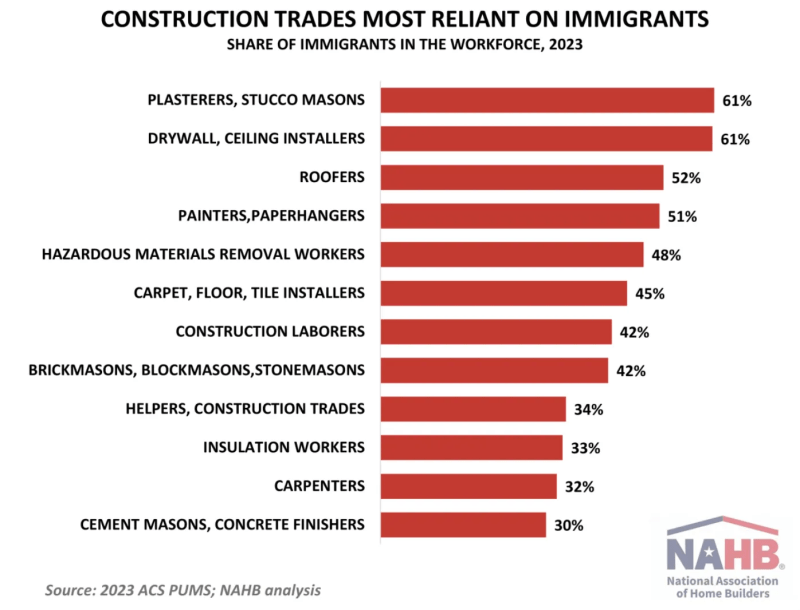

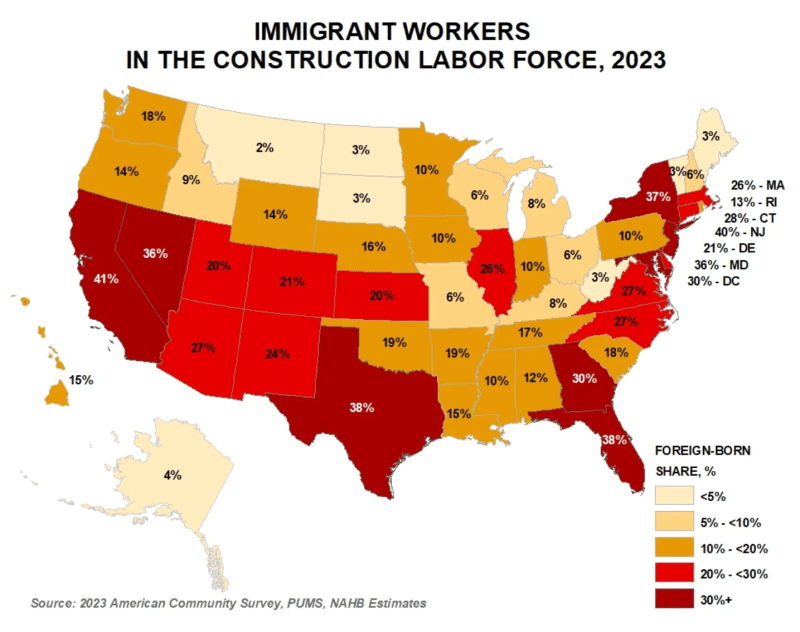

In many states, foreign-born workers make up more than a third of the construction workforce: