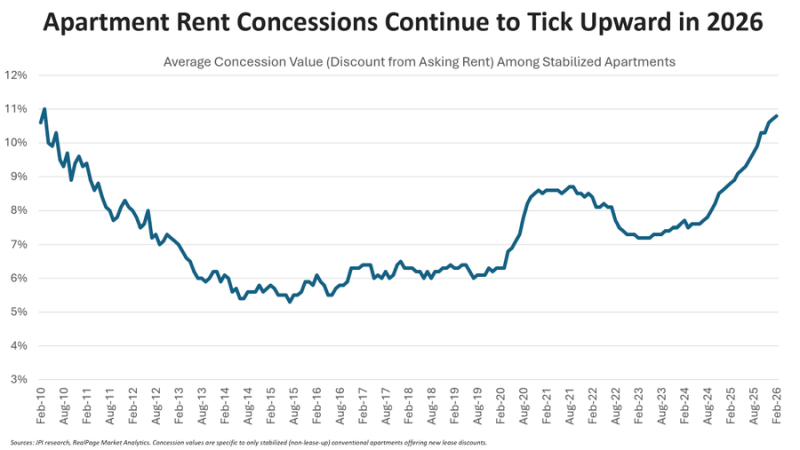

Concessions are at the highest level since 2010, with discounts averaging 10.8% of rent, or 5.6 weeks free.

Source: Jay Parsons

Concessions are at the highest level since 2010, with discounts averaging 10.8% of rent, or 5.6 weeks free.

Source: Jay Parsons

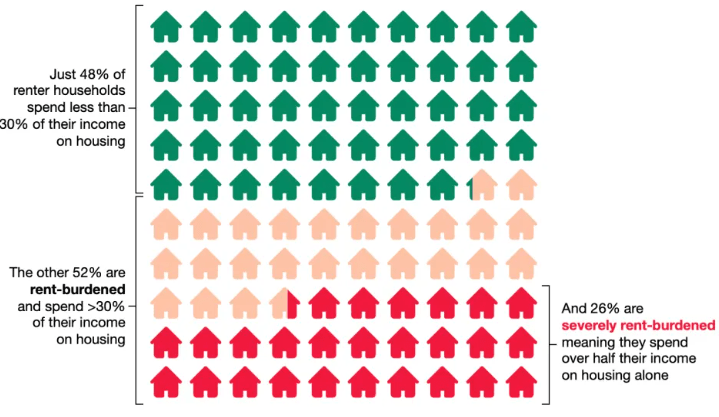

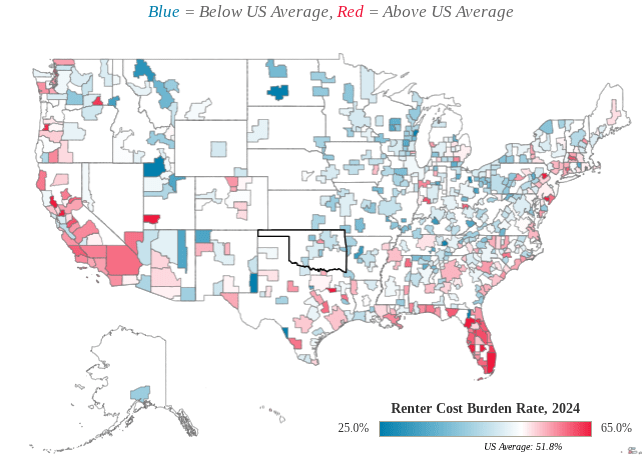

51.8% of all renter households are considered cost-burdened, spending more than 30% of their monthly income on rent.

More than one-in-four renter households spend over 50% of their income on rent, making them “severely cost-burdened.”

In some ways, the cost burden rate could even be underestimating the degree to which housing affordability has worsened. A lack of affordability has deterred new household formation in recent years, as Americans are increasingly doubling up with family or roommates to save on housing costs. These individuals are struggling with housing affordability, but because they don’t represent their own households, they are not captured in cost burden statistics.

Additionally, as the affordability of for-sale housing has eroded even more rapidly than that of rentals, more prospective homebuyers are continuing to rent. This subset of renters who have been sidelined from the for-sale market tend to be higher-income, and their presence in the denominator of the renter cost-burden rate could be depressing that rate slightly.

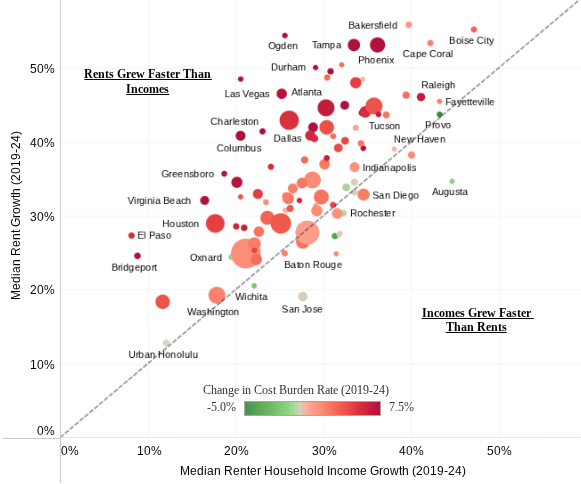

Rents are growing faster than income in 85 of the largest 100 metros:

Source: ApartmentList

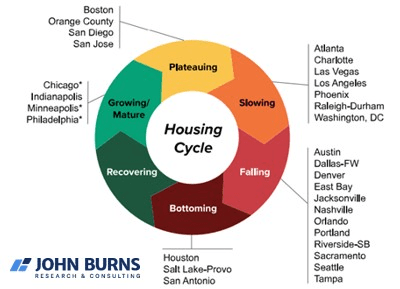

For single-family homes:

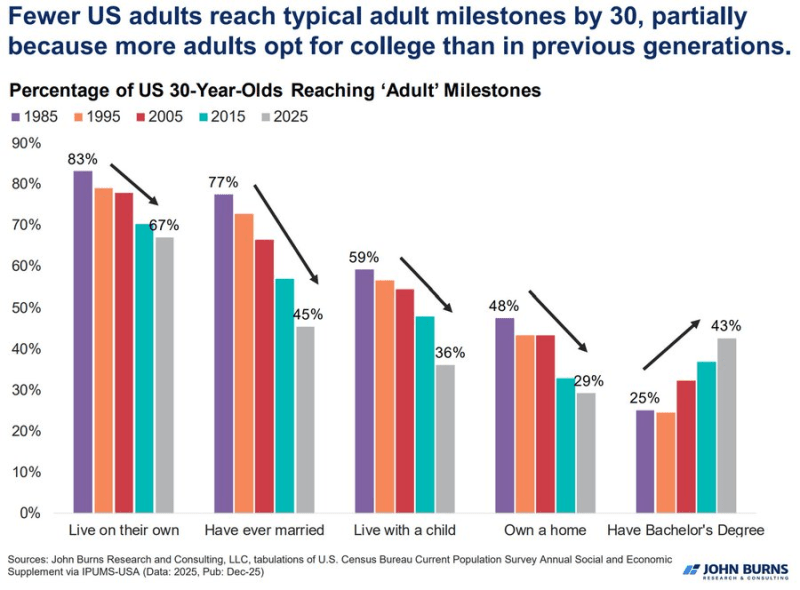

Great chart from showing why the “renting stage of life” is elongating. It’s not just an affordability issue, it’s a decades-long structural shift in Americans waiting longer to get married and have kids (which are the traditional drivers to buying a house).

Source: John Burns and Jay Parsons

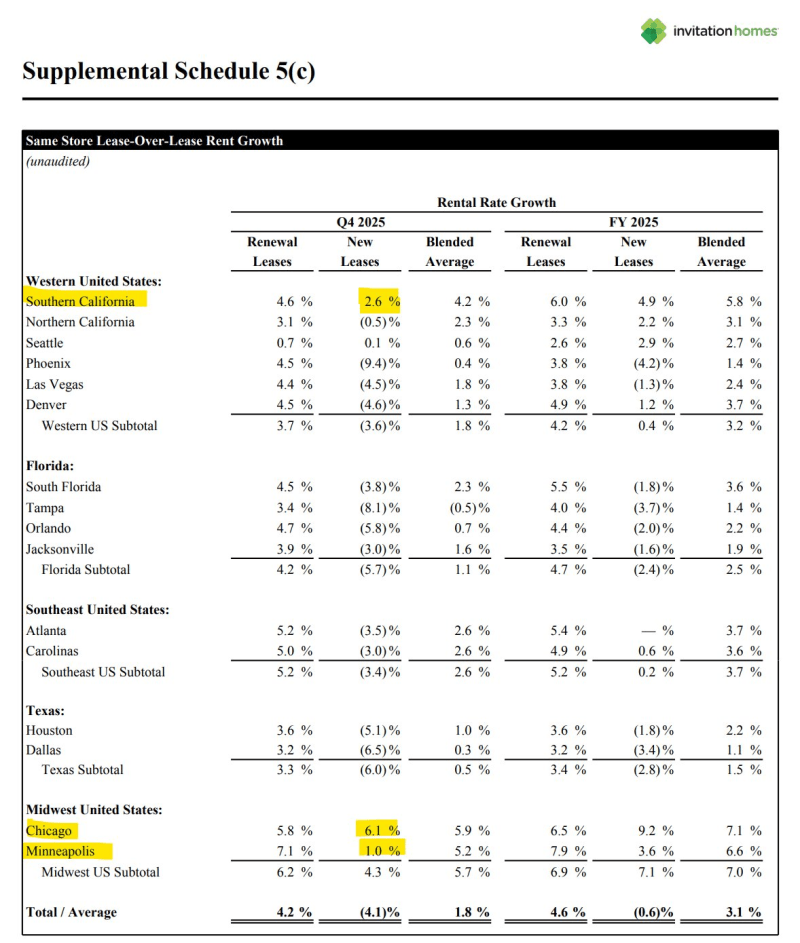

Invitation Homes is the largest single-family home rental company in the U.S. While their renewals remain strong, new lease rents are declining everywhere except SoCal and the Midwest.

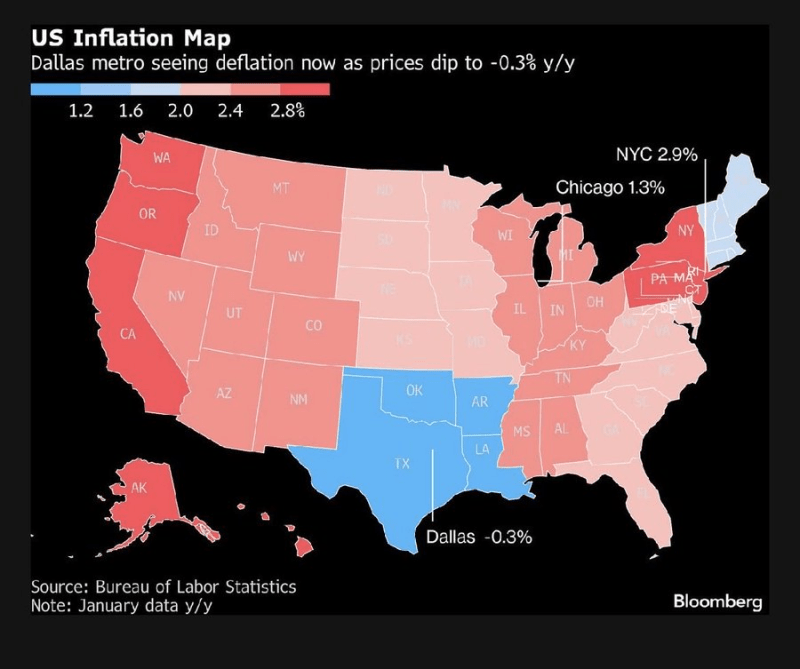

The average CPI of the top 12 largest cities is just 2.2%. Some major cities in the south, like Dallas, are experiencing deflation.

Source: Bloomberg

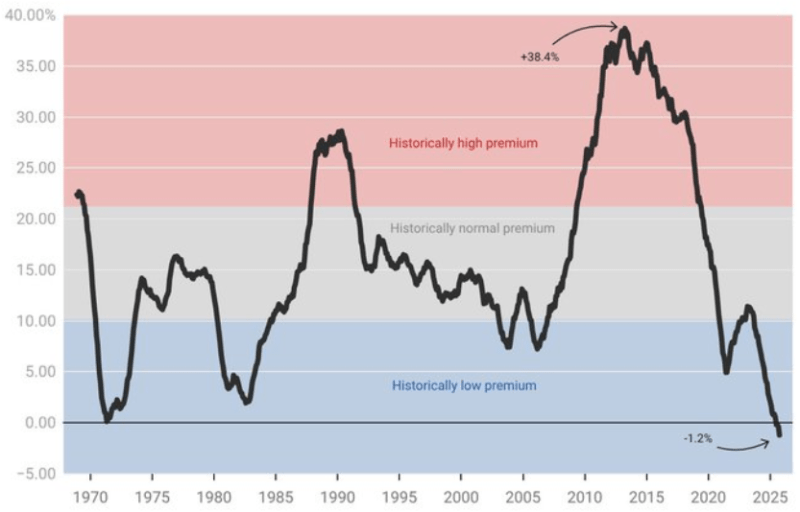

The median sales price of a new single-family home is now 1.2% less than the price of an existing single-family home. This is the lowest premium (now a discount) in history.

Source: ResiClub

REIT stock prices are trading at levels well below net asset value. That makes buybacks more appealing. Bank of America REIT analyst Jana Galan said the REITs are trading at an implied cap rate around 6%. Meanwhile, we’re seeing REIT-quality apartments selling for cap rates ranging from mid-4s to low 5s. That’s a sizable gap that makes buybacks more attractive.

From multifamily REIT earnings calls last week:

EQR’s Mark Parrell said: “The best capital allocation opportunity we see now is to sell properties that we see as having lower forward return profiles and using the sales proceeds to buy back our stock. As you saw in the release, the company purchased approximately $206 million of its stock during the fourth quarter and just subsequent to quarter end for total stock purchases of $300 million in 2025. We see our company with its high-quality asset base and sophisticated operating platform as greatly undervalued in the public markets versus private market values. Also, by acquiring stock with the proceeds from the sales of slower growth properties, we’re effectively improving our forward growth rate as well, a double benefit.”

UDR’s Dave Bragg: “The magnitude of discount to NAV that has persisted in the space just doesn’t happen very often, and we are fortunate that we’ve taken advantage of it so far and plan to continue to do so as we execute on dispositions.”

Camden’s Ric Campo: Once Camden sells its SoCal portfolio, “We also look at the opportunity to redeploy the capital not only in the Sun Belt, but also to buy the shares. And so when we can sell the California portfolio at a cap rate that’s substantially less than our implied cap rate implied in our stock.”

IRT’s Jim Sebra: “Like a lot of our peers, there is a fundamental disconnect between implied cap rates as well as market cap rates. And we looked at that as a good opportunity … to buy back stock.”

Source: Jay Parsons

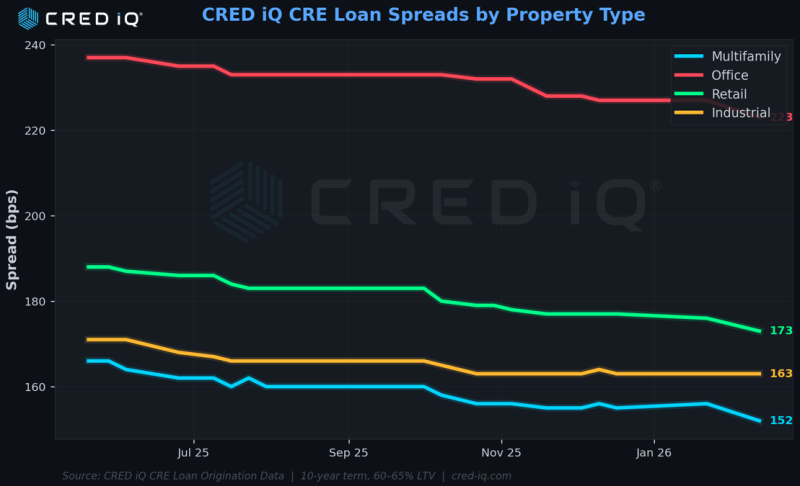

Commercial real estate lending spreads have tightened across every major property type since mid-2025, but the pace and magnitude of compression vary dramatically by sector, and the gap between winners and laggards remains wide.

Multifamily continues to lead with the tightest spreads in the market at 152 basis points over Treasuries, down 14 bps from the 166 bps level recorded in May 2025.

Source: Cred iQ