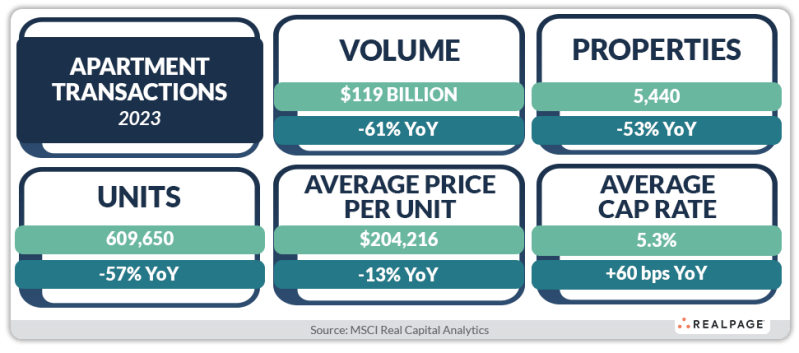

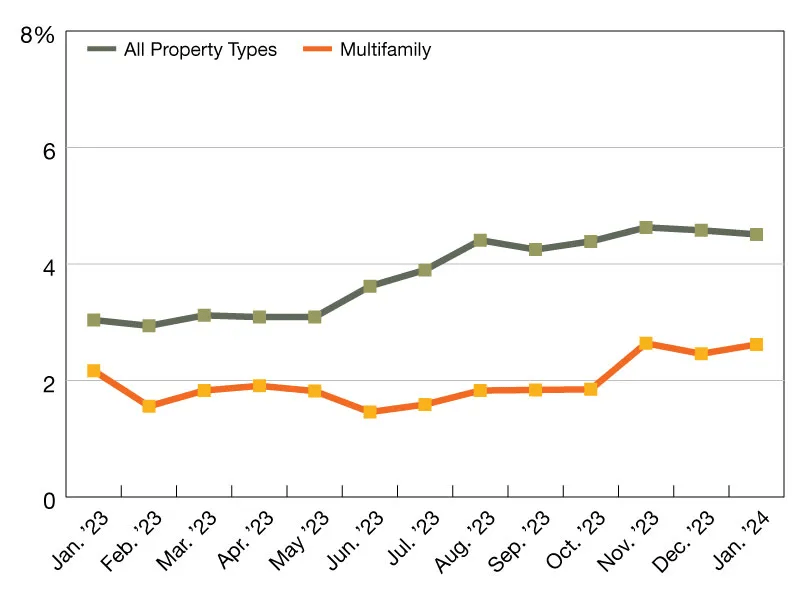

It’s important to note that CMBS loans make up only about 3% of the total $2 trillion in multifamily debt, but we’re offered significantly more transparency to what is happening within this piece of the pie:

Source: Trepp

It’s important to note that CMBS loans make up only about 3% of the total $2 trillion in multifamily debt, but we’re offered significantly more transparency to what is happening within this piece of the pie:

Source: Trepp

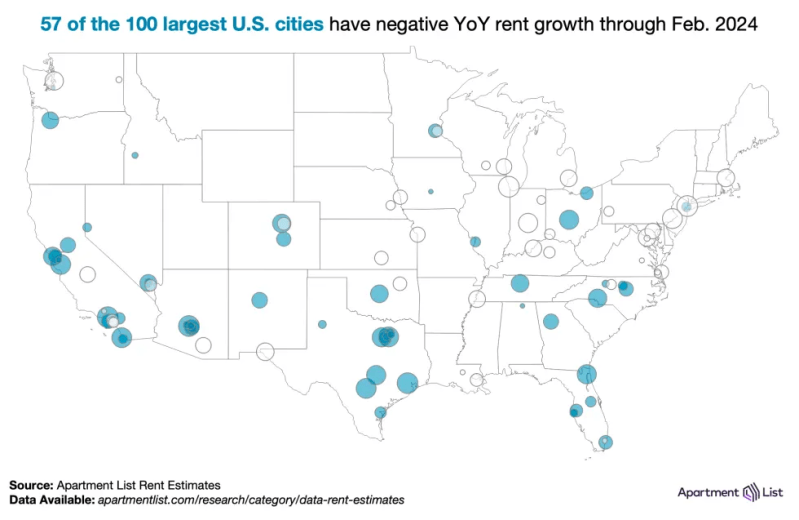

| Source: | Month: | Monthly Change: | Annual Change: | Vacancy: |

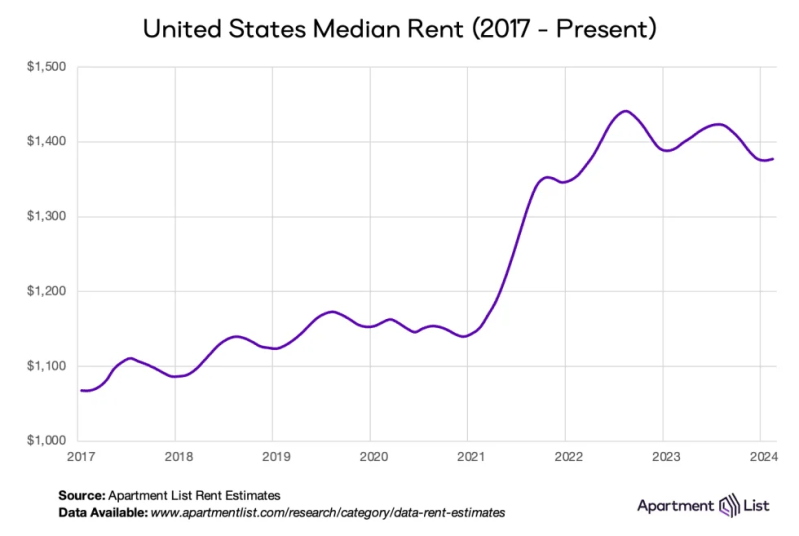

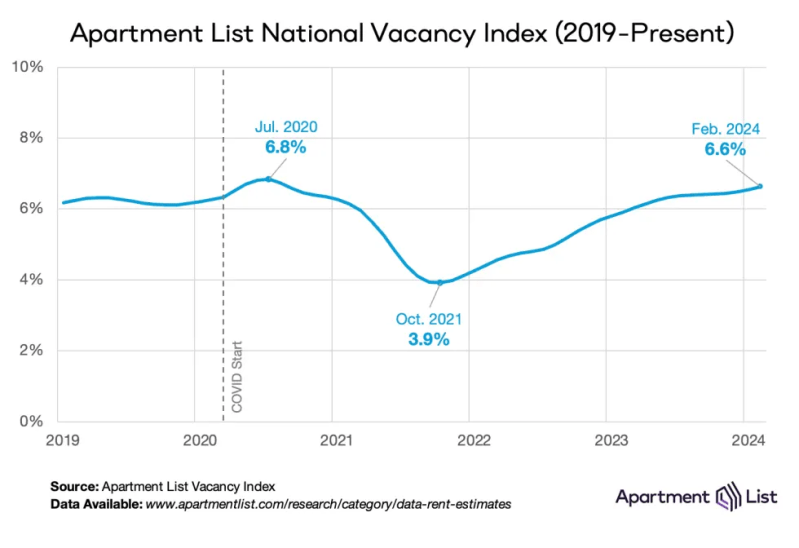

| Apartment List | January | -0.30% | -1.00% | 6.50% |

| CoStar | January | 0.22% | 0.66% | 7.60% |

| Apartments Advisor | January | 0.50% | -2.03% | N/A |

| Apartments.com | January | 0.70% | 0.20% | N/A |

| RealPage | January | N/A | 0.30% | 5.90% |

| Redfin | January | 0.00% | 1.10% | N/A |

| Zillow | January | N/A | 4.70% | N/A |

| Yardi Matrix | January | 0.00% | 0.50% | N/A |

| Rent.com | January | -0.04% | 1.10% | N/A |

| Realtor.com | January | -0.06% | -0.30% | N/A |

| Average: | 0.13% | 0.52% | 6.67% |

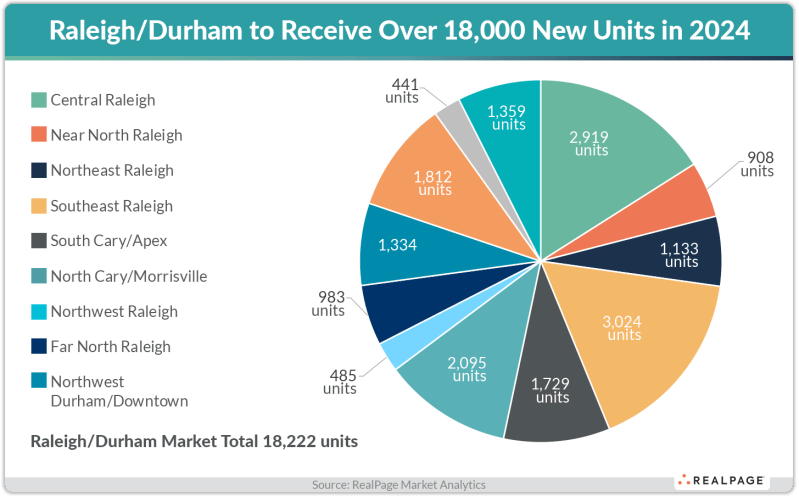

On a previous post I discussed how Raleigh, NC is ranked number 1 on multiple lists as the top market to invest in 2024 using many different metrics.

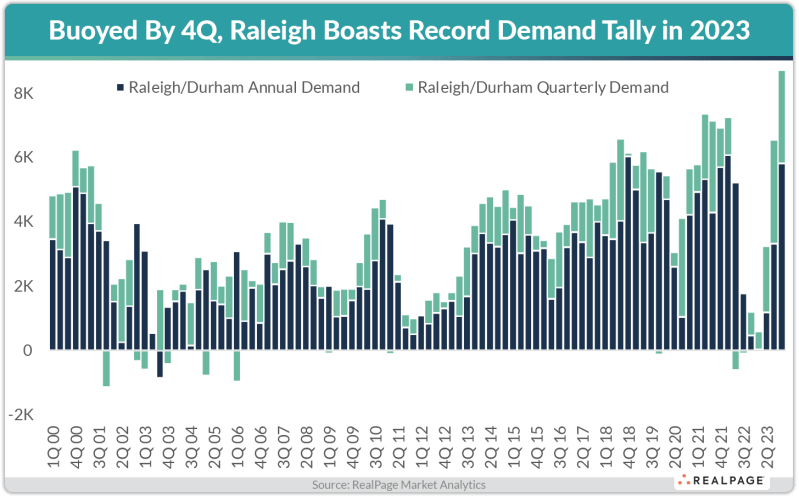

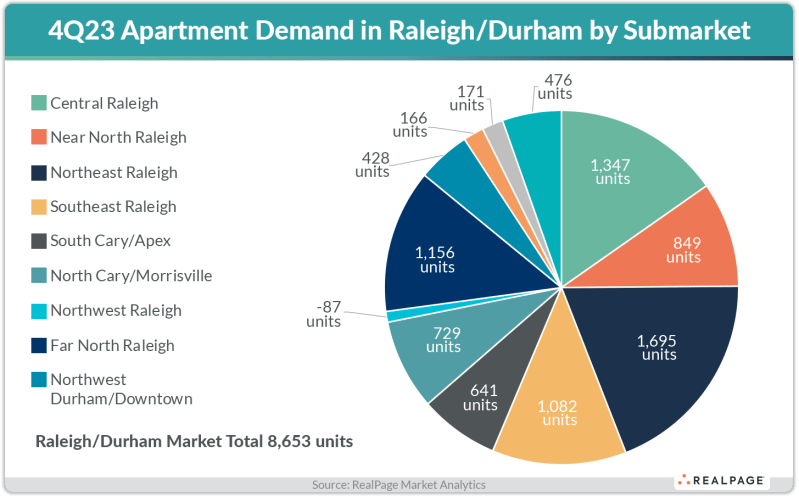

Raleigh’s demand reached an all-time high in the fourth quarter, absorbing 2,886 units. That was more than triple the market’s Q4 average over the last 10 years.

The demand will need to stay strong in order to help offset the supply entering the market this year:

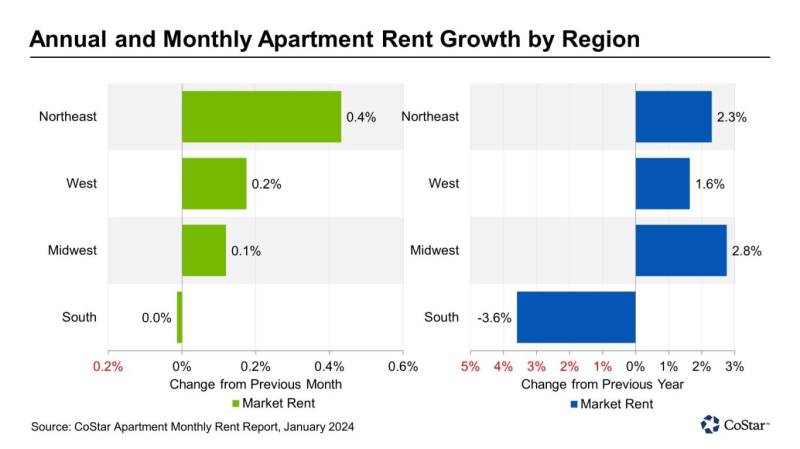

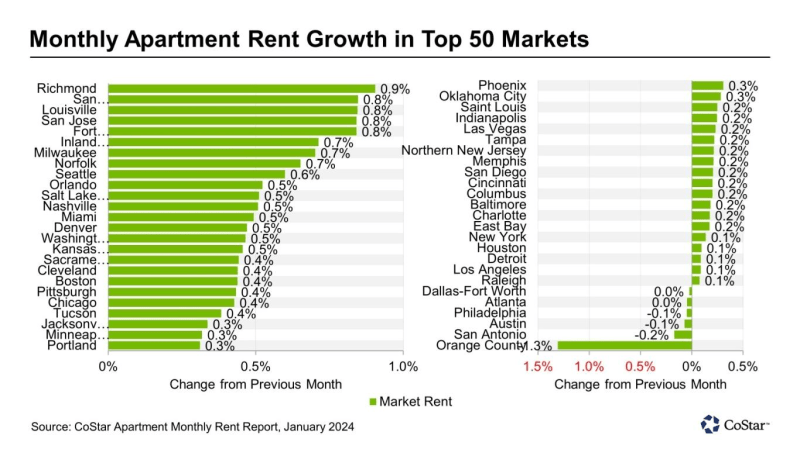

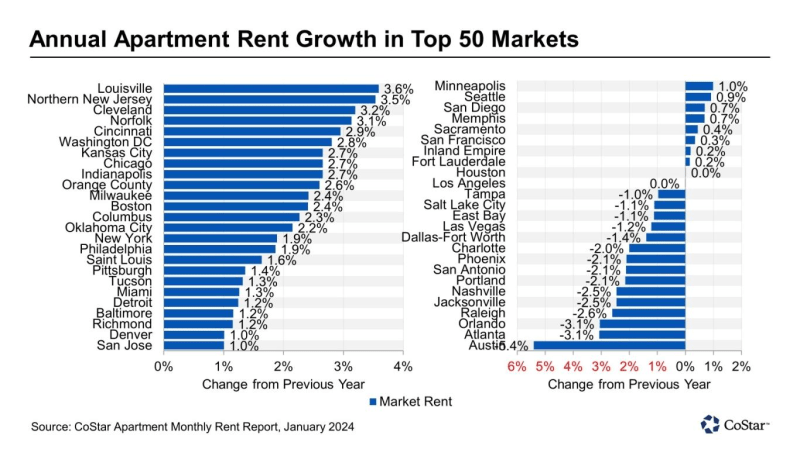

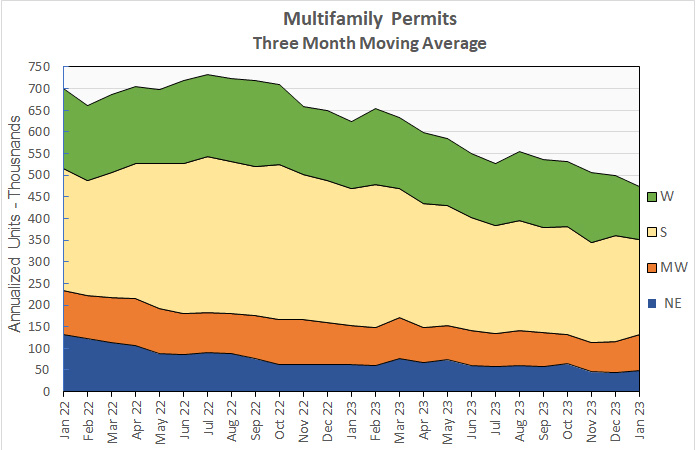

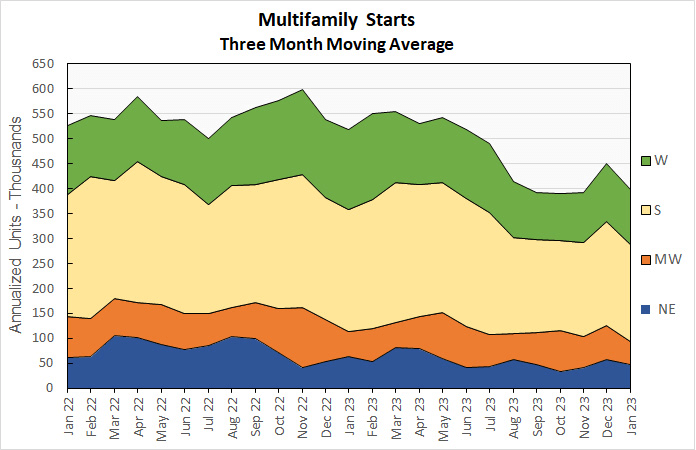

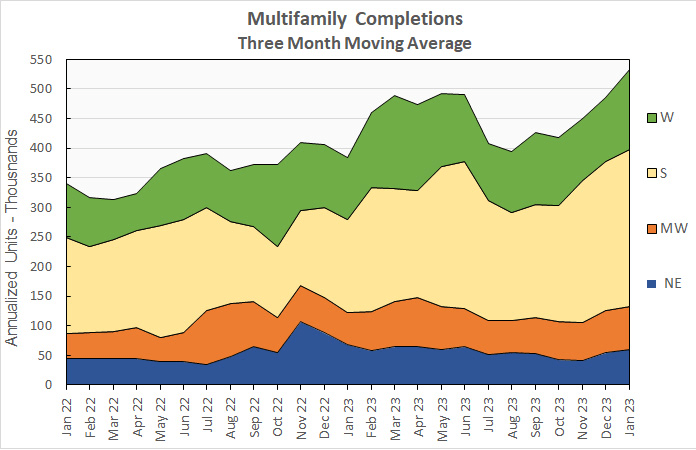

The data below uses a three-month weighted moving average and color codes by region (West, South, Midwest and Northeast):

Source: YieldPro & The U.S. Census Bureau

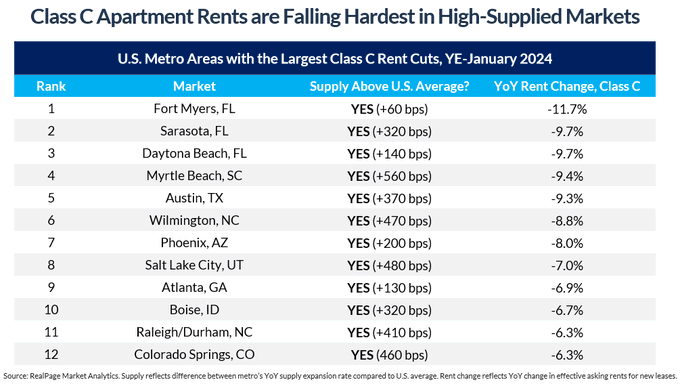

There are 12 markets where Class C rents fell at least 6% over the last year. The new supply of class A units are pulling renters away from class B properties…..and on down the chain.

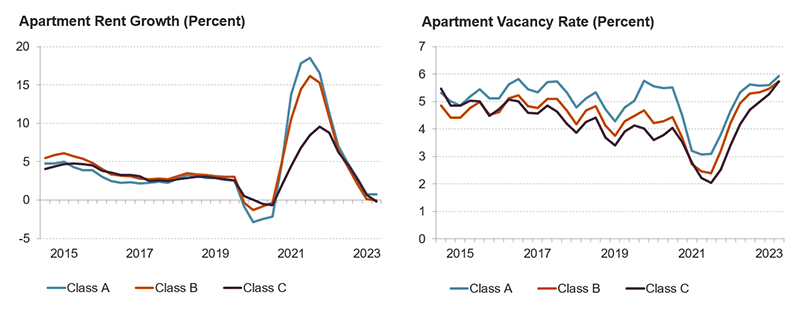

Class C rent growth topped 5% in 18 of the nation’s 150 largest metro areas. All of these markets are regions with little new supply.

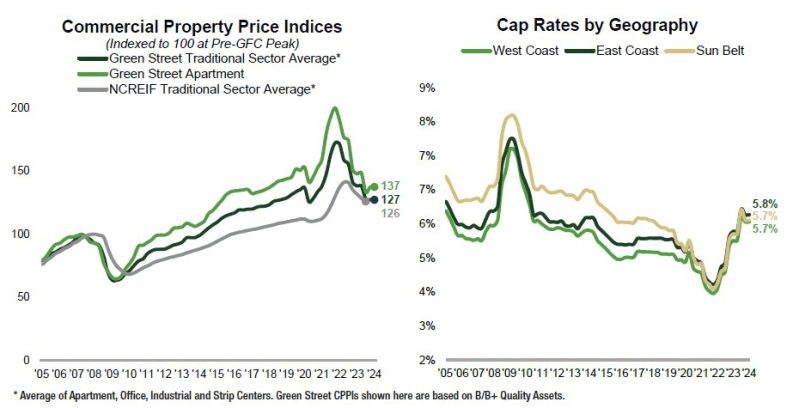

Excess supply helped slow rent increases in previous cycles:

While cap rates have reached 5.7% across the West Cost, East Coast and Sun Belt:

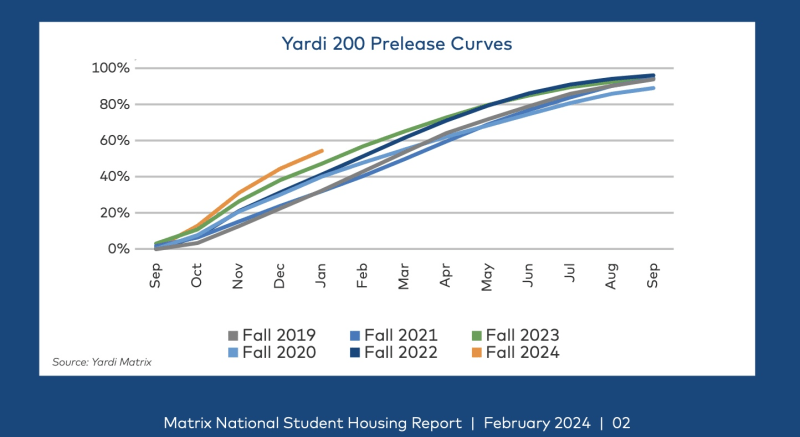

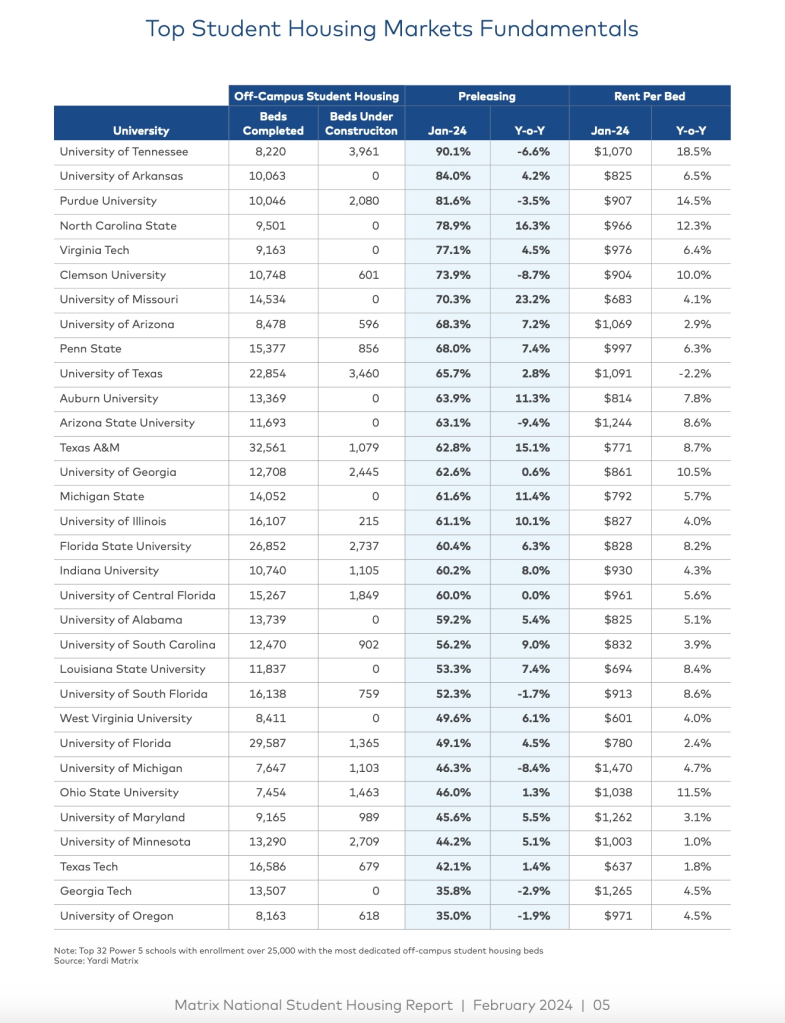

January data continues to show record high preleasing for the 2024 school year:

Snapshot at the top 32 Power 5 schools with enrollment over 25,000 and the most dedicated off-campus student housing beds:

Yardi Matrix anticipates delivery of more than 46,000 new student housing beds in 2024, an increase from the 35,610 beds delivered last year, but expects supply will fall over the next five years to below the long-term average of 36,322 beds per year dating back to 2010.

Student housing investment activity was down last year, with only 76 student housing properties changing hands, compared to an average of 205 in 2021 and 2022. This resulted in a lower price per bed of $75,410 last year, compared with more than $80,000 per bed during the previous five years.

Source: Yield PRO & Yardi Matrix

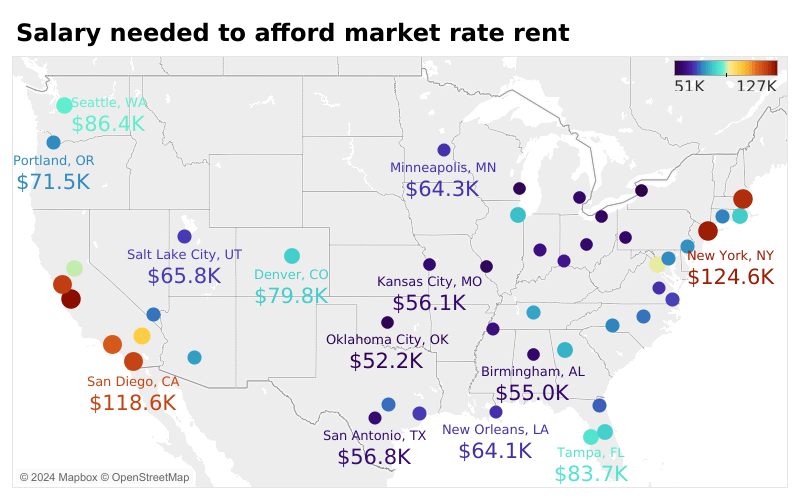

The U.S. News & World Report list is based on the median gross rent and annual household costs for mortgage-paying homeowners of each metro area.

Spartanburg, SC (11) Greenville, SC (12) and Winston-Salem, NC (16) also made the top 25:

Markerr uses machine-learning to accumulate data on real estate markets, and they released their forecast for the markets with the strongest Compound Annual Growth Rate for multifamily rents through 2028:

Markerr analyzed several metrics including population, education, growth of tech workers, and salaried workers in 2011 and compared it to today to try and find where the “next” Austin, TX will be. Raleigh, NC lead the country as the top candidate:

This week Neal Bawa of Grocapitus, a multifamily data analyst, also named Raleigh, NC as his number 1 multifamily market to invest in 2024 based on the outlook over the next 5 to 7 years.

Source: Markerr and Multifamily University