Commercial real estate lenders are done pretending. After years of waiting and hoping that the market would improve, they’re selling off debt on struggling US assets, sometimes writing down as much as 85% of the loan’s payoff amount.

- Lender Ready Capital Corp. offloaded a pool of loans backed by apartments in the Sunbelt at a roughly 30% discount, reducing its exposure to an overbuilt market.

- Ready Capital said in February that it aimed to dump 60% of its legacy commercial-property loan book. It told investors it’s seeking buyers for $1.5 billion of loans, with a focus on clearing non-performing and sub-yielding debt.

- Shanghai Commercial Bank sold its loan on a stalled Manhattan condo conversion at an 85% discount to the debt’s payoff amount.

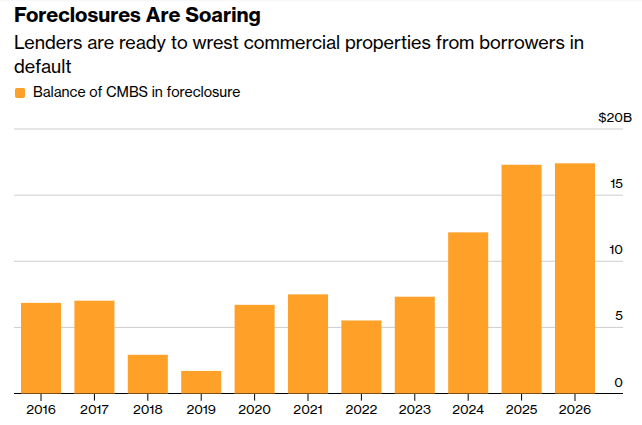

While some lenders are selling off troubled loans, others are moving faster to foreclose. In March, the balance of loans in commercial mortgage-backed securities tied to buildings in foreclosure reached $17 billion, up from $7 billion in 2024 and the highest level since the post-Great Financial Crisis resolution period, according to Trepp.

Parkview Financial recently foreclosed on a pair of apartment towers in Baltimore after the company that converted the former hotel buildings defaulted on its $45 million loan.

Source: Bloomberg