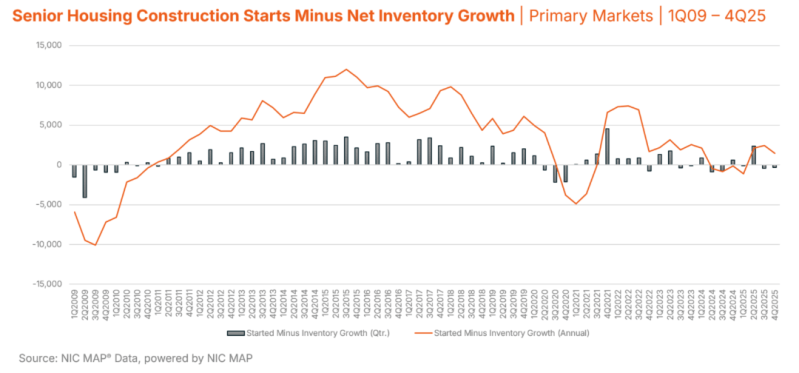

Senior housing construction trends are telling a very clear story. Development activity across the sector has slowed materially, with new inventory growth, active construction volume, and construction starts all trending down.

Combined with accelerating demand, the data suggests that the sector is in a sustained period where supply growth cannot keep pace with the demographic demand forming ahead. The development cycle in senior housing is long, and the projects that are—or are not—starting today will shape the availability of new communities for years to come.

The first indication of this shift appears in the pace of new inventory growth. Annual inventory growth, measured as the net change in operational units, has fallen below 1% for three consecutive quarters. What makes this observation particularly notable is that the slowdown is occurring simultaneously across both Majority Independent Living (IL) and Majority Assisted Living (AL) properties.

There has never been a period when both property types experienced inventory growth this slow at the same time. Over the long history of the sector, development cycles have often varied between property types. Today, however, the slowdown is broad-based.

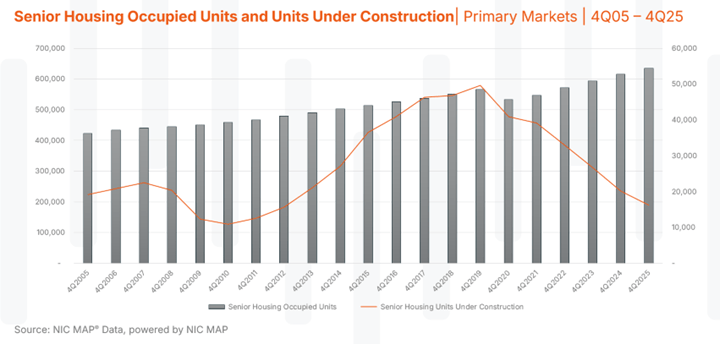

What makes the current level of construction starts notable is how it compares with demand trends across the sector. Absorption—defined as the net increase in occupied units—has remained strong, indicating that demand for senior housing communities continues to grow.

For an industry with a development cycle that can easily span two or more years from planning to completion, the slowdown in construction starts today has long-term implications for the availability of new communities in the years to follow.

At the same time, demographic demand is beginning to accelerate as the oldest baby boomers approach their 80s. Absorption trends across the sector indicate that new residents continue to enter the market at an elevated pace compared to historical norms and at a steady pace in recent years, indicating a new benchmark for annual demand.

This dynamic is already setting the stage for a multi-year supply constraint. With relatively few communities currently under development across many markets, the industry will experience a period where new inventory growth remains limited while demand continues to build. In such an environment, industry occupancy will rise to historic levels, operators gain stronger pricing power, and margins can improve.

Source: NIC Map