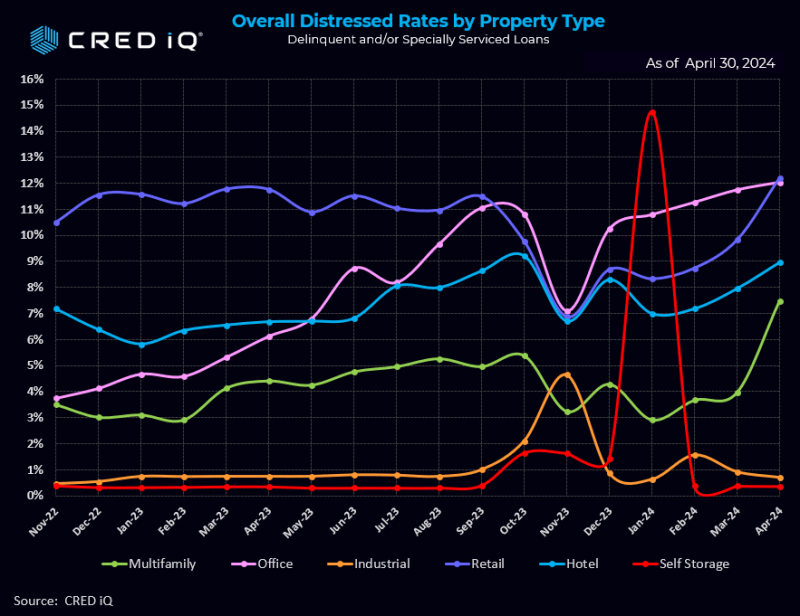

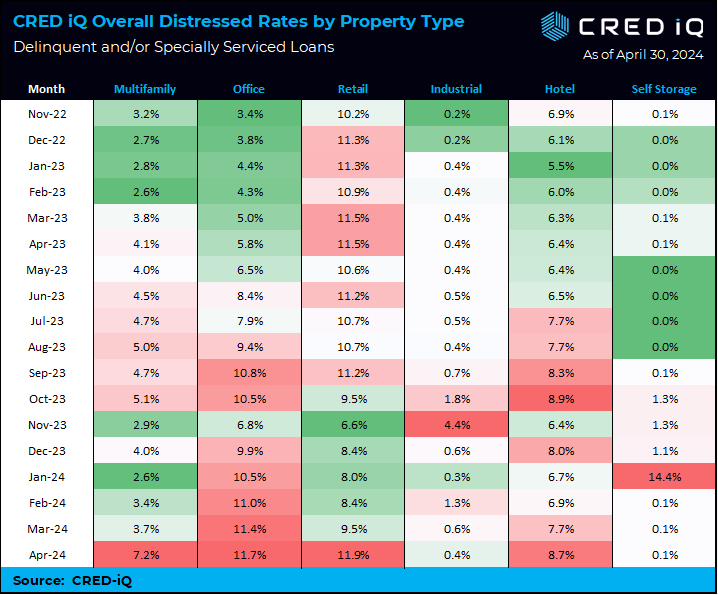

CRED iQ’s distress rate for all property types increased from 7.61% to 8.35%, a 74 basis points jump in April. Multifamily saw a whopping increase distress rate increase – from 3.7% in the March print to 7.2% in April. The increase is mostly attributable to a $1.75 billion loan ($561,000/unit) backed by Parkmerced, a 3,221-unit multifamily property in San Francisco.

CRED iQ’s distress rate aggregates the two indicators of distress – delinquency rate and specially serviced rate – yielding the distress rate The index includes any loan with a payment status of 30+ days or worse, any loan actively with the special servicer, and includes non-performing and performing loans that have failed to pay off at maturity.

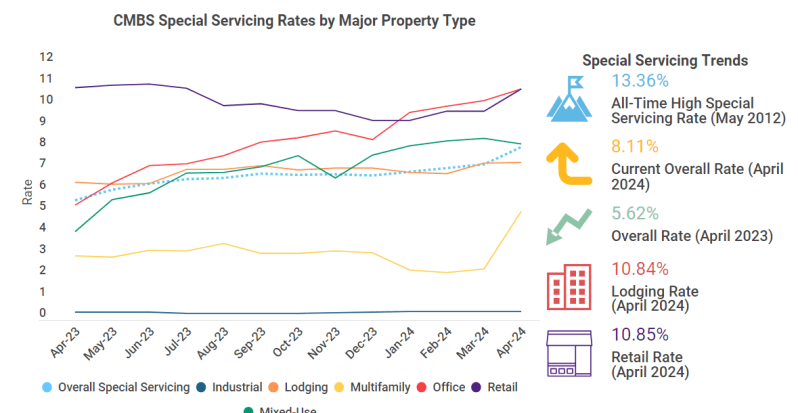

The Trepp CMBS Special Servicing Rate leaped in April, rising 80 basis points to reach 8.11%. This marks the largest monthly jump that the rate has experienced in nearly four years, with higher monthly upticks only reached during the COVID-19 pandemic in mid-2020. The biggest movers were by far ‘Other’ properties and multifamily (yellow line), which increased a whopping 236 basis points and 269 basis points, respectively.

And From Bloomberg:

CRE CLO issuance surged to $45 billion in 2021, a 137% increase from two years earlier, when buyers of apartment blocks sought to profit from the wave of workers moving to the Sun Belt from big cities. Three-year loans would give them time to complete upgrades and refinance, the thinking went.

Fast forward to today and the debt underpinning many of the bonds is coming due for repayment at a time when there’s less appetite for real estate lending, insurance costs have skyrocketed and monetary policy remains tight. Hedges against borrowing cost increases are also expiring and cost significantly more to purchase now.

Those blows helped increase multifamily assets classed as distressed to almost $10 billion at the end of March, a 33% rise since the end of September, according to data compiled by MSCI Real Assets.